Lack of abundant, reliable, and affordable energy is holding back Africa’s minerals sector. Across mineral-rich countries, skyrocketing electricity prices and shortfalls in power supply have raised operating costs, sent mining companies scrambling to secure alternative sources of power, and in some cases even shuttered mining operations.

When these energy challenges make the headlines, the conversation usually centers impacts on western countries’ supply-chain security or ‘green transition’ efforts. What gets far less attention: the strains that power challenges are placing on current mining operations and the gigantic negative impacts on the African economies themselves.

Africa’s mining struggles are power and economic struggles

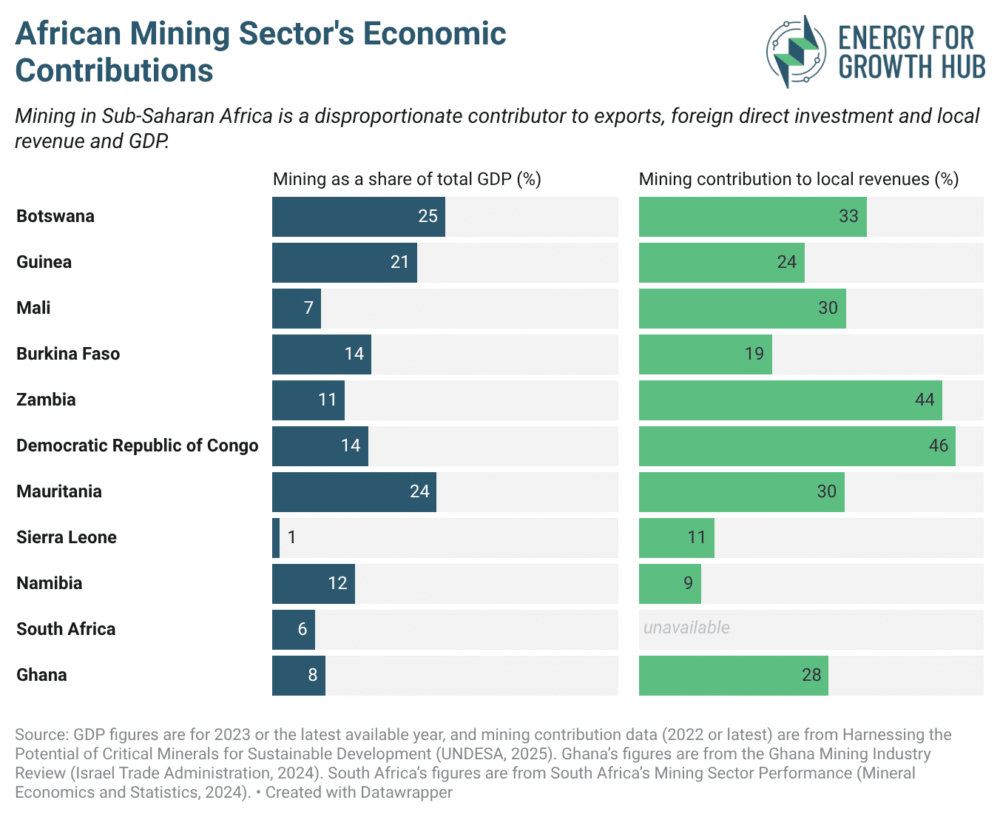

Sub-Saharan Africa’s mining sector, valued at over US$108 billion, is so central to many countries’ economies that its performance shapes overall economic health. In many countries, the sector accounts for half of all exports and the majority of foreign direct investment. Mining contributes a significant share of GDP and makes up a disproportionate portion of the local revenue base of many African countries. As a result, the sector’s struggle to secure reliable, affordable electricity inevitably becomes a national and regional economic struggle.

Electricity shortages in mining → 3 ways African economies lose out:

- Job losses. Across Africa, unreliable and costly power is costing mining sector jobs. In South Africa, rising electricity prices and frequent outages have triggered thousands of job losses across the ferrochrome and vanadium industries. These job disruptions extend beyond local employment, hurting global energy and transportation manufacturing sectors that rely on them. Steel giant ArcelorMittal South Africa has warned that rising energy costs could trigger 4,000 layoffs, nearly half its workforce. Mozal, Africa’s second-largest aluminum producer and a major power consumer, has announced it will close its smelter in Mozambique after failing to agree on cheaper electricity prices with the government. This will erode the continent’s limited smelting capacity and eliminate value-addition jobs, which tend to pay higher than those in extraction. Job creation is already a top concern for African countries. This doesn’t help.

- Less local value addition. Many African countries would like to do more than export raw materials: they want to process more minerals at home and use their mineral wealth to build local manufacturing. This won’t make sense everywhere. But electricity shortages are one key factor making it much harder. In Ghana, the lack of reliable power makes lithium refining prohibitively expensive. And in South Africa, the world’s largest ferrochrome producer, the rising cost of electricity (which constitutes the single largest cost in ferrochrome production) has pushed producers to abandon smelting efforts and export raw material instead. A similar trend in the iron ore sector is further entrenching the lack of producer diversity and a system that prioritizes ore exports over steel production. This locks African economies into low-value economic activities, undermining prospects for often-aspired value addition and local wealth creation from mineral resources.

- Utility revenue loss and death spiral. Mining is a major energy consumer; accounting for ~20% of Africa’s total electricity consumption in 2024 (assuming mining represents about half of industrial electricity consumption). In some countries, like Zambia and Mozambique, this share rises to as much as 50%. This makes Africa’s power utilities, which are already deeply financially insecure, highly sensitive to disruptions in the mining industry. In Mozambique, the potential shutdown of an aluminum smelter would risk more than $300 million in annual revenue for the national utility. And in the DRC, the national utility lost about $4 billion in revenue between 2019-2023 because electricity shortages forced mining companies to either import power from South Africa or rely on backup generators. Across these countries, utilities rely on large industrial consumers for bulk electricity purchase and dependable revenue. As more of these big mining customers are forced to go off-grid, utility performance may decline or tariffs may go up to close the financial gap, worsening conditions for other commercial and residential consumers.

Power constraints are defining Africa’s mining present and future

As the world debates future pathways to supply-chain diversity, costly and unreliable power is already costing African jobs, revenue, and deepening the continent’s vulnerabilities and economic prospects. Africa’s mineral wealth may, in theory, fuel the world’s energy future, but without abundant and affordable power to fuel these ambitions, extraction will falter and any downstream opportunities — for African economies and global supply chains alike — will vanish. African policymakers must therefore insist that energy policy sits at the core of mining policy. If Africa is to maintain current mineral production, let alone expand it, international partners must also advance energy abundance.