The DFC is chronically torn between its dual mandates of promoting development in the poorest nations and backstopping other US national security interests. The BUILD Act that created the agency was explicit that priority should go to projects in low- or lower middle-income economies. So one way to assess the DFC’s balance is to parse its commitments by income groups. But parse what specifically? What’s the best way to assess the DFC’s performance on development?

Todd started by raising a red flag that the majority of DFC’s investment dollars were going to upper-middle or high-income countries, not the priority poorer markets. Andy fired back that loan volumes were less important than project numbers, and that using dollar volume as a measure could create disincentives for loan officers to fund small, high-impact projects. We now agree (boring!) that both dollars and project numbers are useful indicators, taken in context.

How DFC allocates its internal program dollars

Yet there’s a third, important metric: how DFC is allocating its precious foreign aid resources to “buy” the financing that the US Treasury ultimately provides for projects (we’re about to explain). Some context that’s confusing to almost everyone:

- DFC does not actually issue its loans. Like every other US government agency (e.g., the Small Business Administration or federal student loans) the US Treasury is the lender and guarantor. Other agencies essentially buy these loans or guarantees from the Treasury similar to the way a consumer pays a premium to buy car insurance. The premiums are paid to the Treasury out of each agency’s annual appropriation.

- How much DFC has to “pay” to Treasury to issue a loan or guarantee depends on risks, interest rates, and fees. DFC uses a US government formula to calculate the “credit subsidy,” which is the amount that an agency must pay for each transaction. Treasury looks at country risk (a loan in Haiti may cost an agency more than one in Mexico), borrower risk (a start-up company with no credit history will require a higher credit subsidy than a creditworthy one), and market risk (a nascent market, unpredictable sector, or a newer technology will cost more than established ones). Treasury also considers the loan’s interest rate, fees, and length. If the loan is deemed likely to pay a decent rate and unlikely to default, Treasury charges DFC nothing to issue that loan. If the loan or guarantee is risky, Treasury will ask DFC to cover the difference with a credit subsidy paid out of DFC’s programmatic budget. That programmatic budget used for subsidies is considered foreign assistance and reported on USAspending.gov.

- DFC can use its programmatic budget to drive impact. DFC can use its programmatic budget, which is used to cover both credit subsidies and grants, to make a project cost less to the investor or to boost its development impact beyond what a pure market rate would achieve.

- DFC’s equity investments also come from DFC’s programmatic budget and require credit subsidies. DFC has the authority to make direct investments in companies (rather than loans or insurance), but under current budget rules, equity investments are counted like grants as part of DFC’s programmatic budget. For this reason, using DFC’s programmatic budget to support a loan subsidy vs. an equity investment is a zero-sum game in that the money comes from the same pool of programmatic money. So any analysis of credit subsidies for loans and guarantees should be done alongside DFC’s investment in equity instruments.

If this all sounds like excessive government intervention, we do it all the time. We subsidize health insurance for elderly cancer patients because we want everyone to have affordable coverage and we subsidize farmers because we don’t want rural communities to collapse in a bad year. Similarly, DFC can use its programmatic budget by spending more of its funds to bring down the cost of lending for a $10 million farm expansion or a $200 million power plant in Nigeria because we want to encourage food security and access to electricity for everyone. A project in Colombia may cost DFC nothing extra because it will be seen as low risk and will earn interest and fees, but for the same project for the same loan amount in Nigeria, DFC could be charged a small percentage of the total. Using its programmatic budget for “subsidy” is one way DFC can drive impact in poorer countries and riskier projects.

DFC is limited by the size of its total programmatic budget, which last year was $780 million to cover credit subsidies, equity investments, and grants. Note that this programmatic budget is different from the $60 billion maximum contingent liability provided by Congress. That $60 billion is like a credit card limit, and Congress can raise it at any time.

Although DFC’s programmatic budget is technically paid by taxpayers, that’s only because DFC does not retain its own profits; in past years, the agency has paid more into the Treasury than it receives.

DFC’s equity investments are treated like grants from a budgetary standpoint which means that DFC has to pay the Treasury $1 for every $1 it makes in an equity investment. Consequently, DFC currently gets much greater leverage from its subsidy budget for loans, guarantees, and insurance, which typically require DFC to pay a very small percentage or even nothing to Treasury to issue the loan, grant or insurance product. (If the budget rules for equity are changed, as many hope, this would also change, not only allowing more equity but also freeing up resources for more high-impact lending.)

So one way of assessing DFC’s development commitment is how it allocates its programmatic budget, particularly the subsidies. Unfortunately, the two public DFC project databases don’t contain this information, but the USAspending.gov portal does. For example, DFC provided a $9.5 million loan to Apollo Agriculture in Kenya — a lower-middle income country. For Treasury to provide DFC with that guarantee, DFC had to pay nearly $2.8 million. That project will provide loans to farmers, encouraging higher developmental impact. By contrast, for a $55 million car financing facility that DFC established in Colombia, it did not have to pay the US Treasury anything to issue the loan.

The data says…

We pulled all the project data and segmented subsidies by income groups for fiscal years 2020, 2021, and 2022. Here’s what the data says:

- In project number terms, 71% of subsidized loans and 85% of equity investments were in LICs or LMICs.

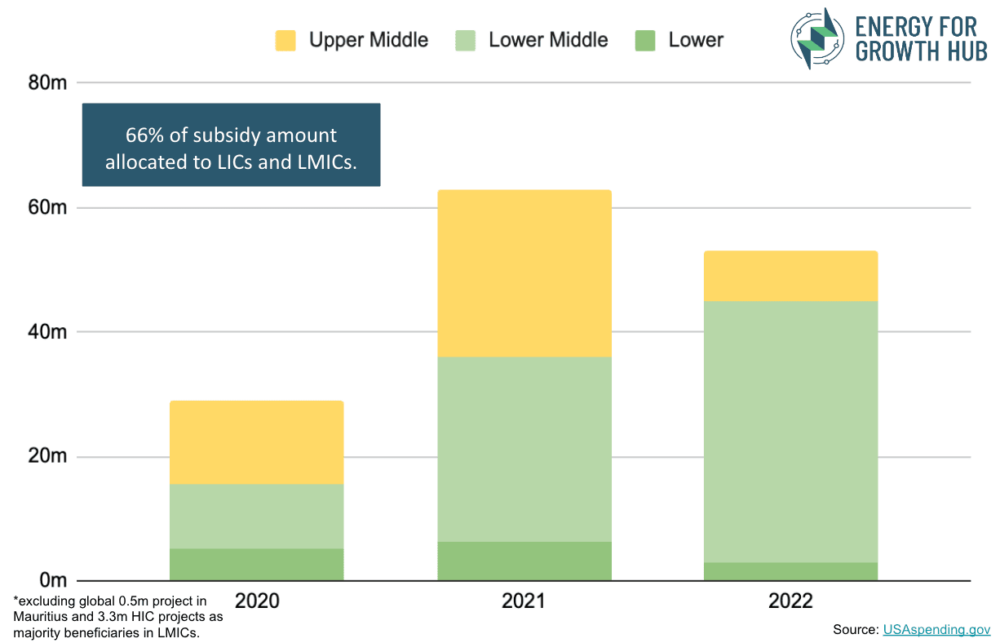

- In dollar terms, 66% of loan subsidies (Figure 1) and 82% of equity investments (Figure 2) were in LICS or LMICs.

- Across combined loan subsidies and equity investments in dollar terms, 80% of combined loan subsidies were in LICs and LMICs (Table 1).

Conclusion

Precious subsidy and equity dollars are mostly being directed toward the lower-income countries that comprise DFC’s priority markets. This indicator is worth watching in light of potential future changes in the US budget scoring system. However, while DFC’s portfolio increased in dollar volume in FY 2023, the total number of projects it supported declined. DFC should continue to use its programmatic resources to support even more deals in lower-income countries.

FIGURE 1: DFC subsidized loans, subsidy amounts in US$

FIGURE 2: DFC equity investments, US$ amounts

TABLE 1: DFC loan subsidies and equity investments