Transparency is perhaps the cheapest and most systematic way to reduce perceived risk premia (which may be based on misconceptions) and make energy and infrastructure markets in emerging and developing economies (EMDEs) more efficient. Transparency lowers financing costs, which CAPEX-intensive low-carbon technologies are especially sensitive to and already face premiums for.

The GEMs database is a crucial source of risk insights–but few lenders have access

The Global Emerging Markets (GEMs) Risk Database Consortium is a credit risk transparency initiative led by 27 Multilateral Development Banks (MDBs) and Development Finance Institutions (DFIs). It pools anonymized data on how over 15,000 loans to 10,000 public and private clients in EMDEs–collectively worth more than $1 trillion across more than 120 countries–have performed over the last 30+ years.

Especially in data-scarce frontier or conflict markets, GEMs data is often the most comprehensive source of credit data available and can help MDBs and DFIs benchmark their performance, improve their provisioning estimates, and calibrate their risk models.¹

The GEMs database is crucial because information on credit performance in EMDE markets remains notoriously fragmented and opaque. Where standard global credit bureaus and commercial data providers focus on major markets, GEMs offers information that is often critical for appraising infrastructure investments in some of the most challenging risk environments.

The problem is that private lenders do not have access to this data, leaving them in the dark–and largely on the sidelines–when it comes to allocating and deploying capital in EMDEs. This lack of data is one of many factors limiting private clean energy finance flows to a tiny fraction of what’s needed. It also pushes public institutions and commercial banks to compete with each other in countries and sectors with less overall risk, which both limits the financial additionality of the public capital being deployed and restricts capital flows to the riskier markets and sectors.

Without good data, lenders often bake overly conservative assumptions into their underwriting models, inflating the cost of capital and slowing the pace of project deployment. These premiums can be prohibitively expensive; from 2013-2023, EMDE issuers paid estimated average credit premiums of about 250-1000 basis points (bps) on US issuers with the same credit rating. See Figure 1.

More widespread access to GEMs data could unlock risk mitigation strategies, lower capital costs, and help scale up climate finance in places where it’s needed most.

Transparency is increasing…but more is needed to make a real impact on lending.

There is a strong general consensus among MDB shareholders, credit rating agencies, think tanks, and private investors that greater access to this database will help private capital allocators better assess and price risk in markets where they would otherwise be unlikely to invest.

To this end, the GEMs Consortium has released a series of high-level reports and summary datasets over the last few years. (Unfortunately, these have been accompanied by relatively little fanfare outside the wonkiest of development finance circles.) This is a significant and necessary step forward, but these releases have thus far been too aggregated across sectors and regions to be decision-useful for investors.

What have we learned so far?

While not yet usable for underwriting transactions, the increased transparency has uncovered some important trends in lending in EMDEs:

1. Perceived risk > real risk

Despite some formidably large benchmark country risk premia, the consortium’s lending to public and sovereign clients has been remarkably low risk (arguably too low), with an annual average default risk of just 1.06%. Loans to the private sector have also performed better than market expectations, with a portfolio average default rate of 3.6% between 1994 to 2023, roughly comparable to a single B (S&P Ratings) / B3 (Moody’s) rating.

This means emerging market corporates (at least, those who can raise financing from the official sector) generally straddle the low end of investment-grade credit and the high end of high-yield credit in advanced economies, challenging the assumption that emerging economies inherently carry higher default risk – and the common assumption that sovereign credit ratings are a suitable proxy for private credit risk in the absence of more granular data.

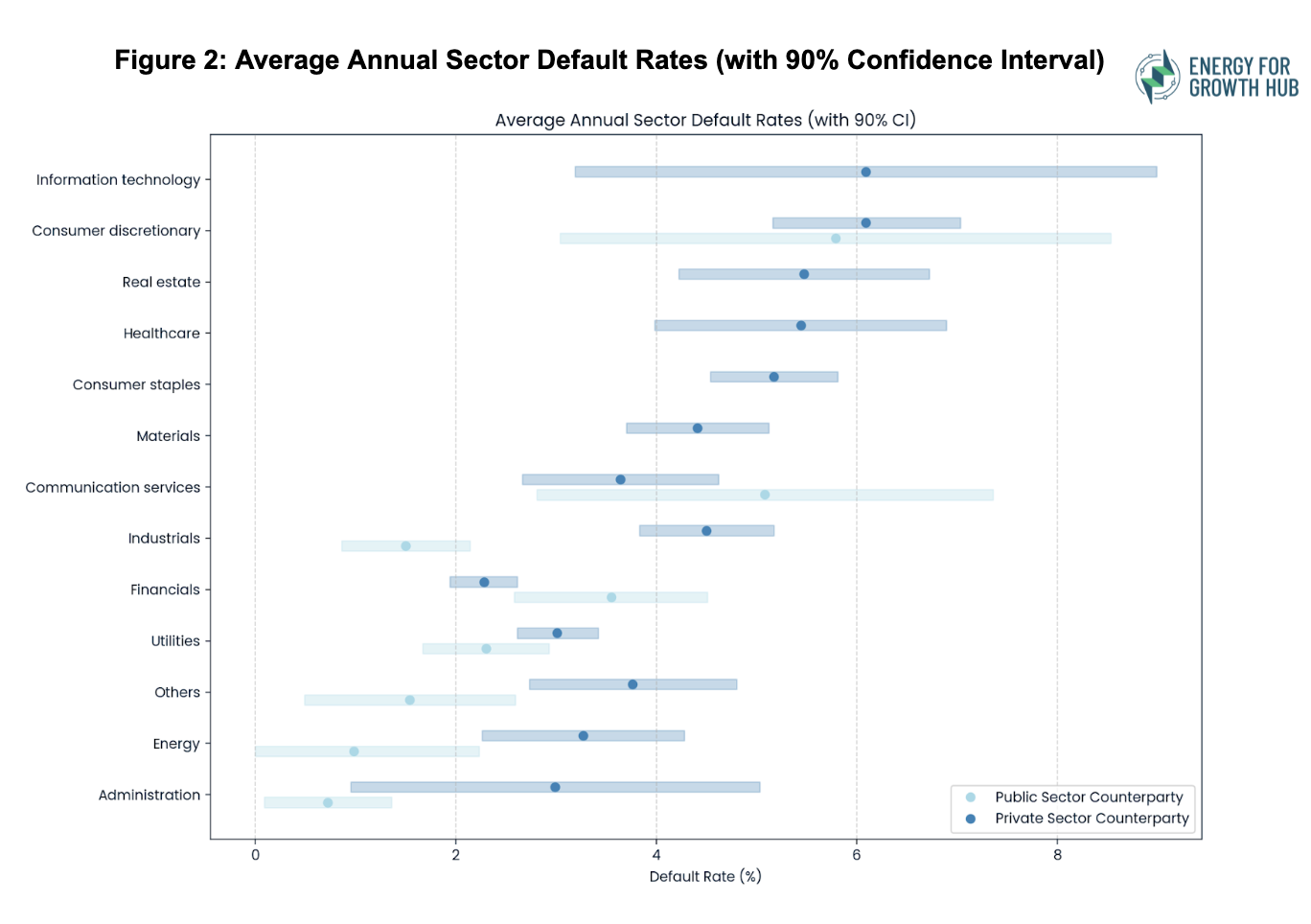

2. The energy sector’s credit performance stands out

Loans to private sector energy and utilities companies have performed especially well relative to other sectors, with default rates below the 3.6% portfolio average, even with a higher-than-average share of recipients in lower-income countries. See Figure 2.

This means that as global capital markets increasingly allocate towards infrastructure, EMDE private energy assets could help diversify risk-off portfolios for the likes of pension funds and insurance companies.

3. Sovereign ratings grossly overstate default risks in low-income regions.

The data show that default rates on private borrowers decline with income level but are consistently lower than those implied by sovereign credit ratings in all but high-income countries. In low-income countries, the actual default rate (6.3%) is significantly below the 14.2% rate implied by sovereign ratings, challenging assumptions about excessive risk in these markets. See Figure 3.

This means that relying solely on sovereign credit ratings may cause investors to overestimate the real risk of private sector lending in low-income countries. Of course, these default rates reflect the risk profiles of projects with Consortium member participation, which benefit from preferred creditor status, deep political relationships, and powerful shareholders; benefits that are not necessarily widely available in the market.

Source: “Reassessing Risk in Emerging Market Lending: Insights from GEMs Consortium Statistics.” IFC Research Note, October 2024.²

To improve transparency in EMDE lending portfolios, the GEMs Consortium could:

- Publish more details: This could include disaggregated default and recovery data by country, sub-sector, year, tenor, and key contractual terms, wherever sufficient data exists. This level of detail is essential for private investors and credit rating agencies to make differentiated, evidence-based risk assessments. The G20 has taken a leading role in advocating for this disaggregated, publicly-available database, dubbed GEMs 2.0, and it’s made its way into myriad global declarations since then.³

- Expand the consortium: Broader participation could capture a larger share of EMDE climate-aligned infrastructure debt, ensuring broader relevance and representativeness, making it a more complete and credible reference point for EMDE infrastructure credit risk.

- Tell more investors: Promote GEMs much more actively—nearly two-thirds of private investors surveyed in 2024 had never heard of it, yet 80% found it valuable once they were informed.

- Include context on the probability and drivers of default: Including context on assessed probability of default and why defaults occurred makes the data more actionable and improves the predictive power of credit assessments.

- Encourage GEMs data use by Credit Rating Agencies: Actively engage credit rating agencies to integrate GEMs data into their sovereign and project-level methodologies, improving the realism and relevance of credit benchmarks in EMDEs.

Most importantly, this data underscores the importance of a similar (or perhaps even greater) level of transparency needed for equity deployment, not just debt, as equity is the foundation of the capital stack.

Conclusion

By releasing and standardizing more of the GEMs data, the consortium can dramatically improve the assessment and pricing of emerging market energy and infrastructure credit risks—particularly for clean energy. Lowering the risk premium for these projects would drive down costs and catalyze substantial increases in investment flows, accelerating the transition to a low-carbon future in regions that stand to gain the most.

Endnotes

- Specifically, models known as probability of default (PD) and loss given default (LGD) models.

- Note: The light blue bars represent the average default rate in the GEMs sample (1994–2023) by country income group (from the 2024 World Bank Group country income classification). The navy blue bars display average default rates implied from historical country sovereign ratings from 1994 to 2023 for the same county groups (subject to data availability). Historical default rates implied in country sovereign ratings are from Standard & Poor’s (2024): “Default, Transition, and Recovery: 2023 Annual Global Sovereign Default and Rating Transition Study. March 2024”.

- The proposal garnered broad support: it was endorsed or welcomed in the 2022 Bali declaration, the chair’s summary at the World Bank 2023 Spring Meetings, the 2023 Paris declaration, the latest G20 finance ministers’ statement and the recently issued G20 report on multilateral development bank reform, to name a few.