Last year, we noticed a growing number of energy infrastructure press releases linked to mining activities in Africa. Unreliable and costly grid-connected power has been a major pain point for mining operators in resource-rich African nations. Knowing this, we expected to find lots of announcements about on-site, self-generation power projects to avoid the grid. But upon a closer look, three surprising trends float to the top. First, the mining sector’s power demand is large, even if poorly quantified. Second, mining firms aren’t leaving the grid entirely; they are hedging it with parallel power systems. Third, decision makers are attempting to respond with limited visibility into these dynamics.

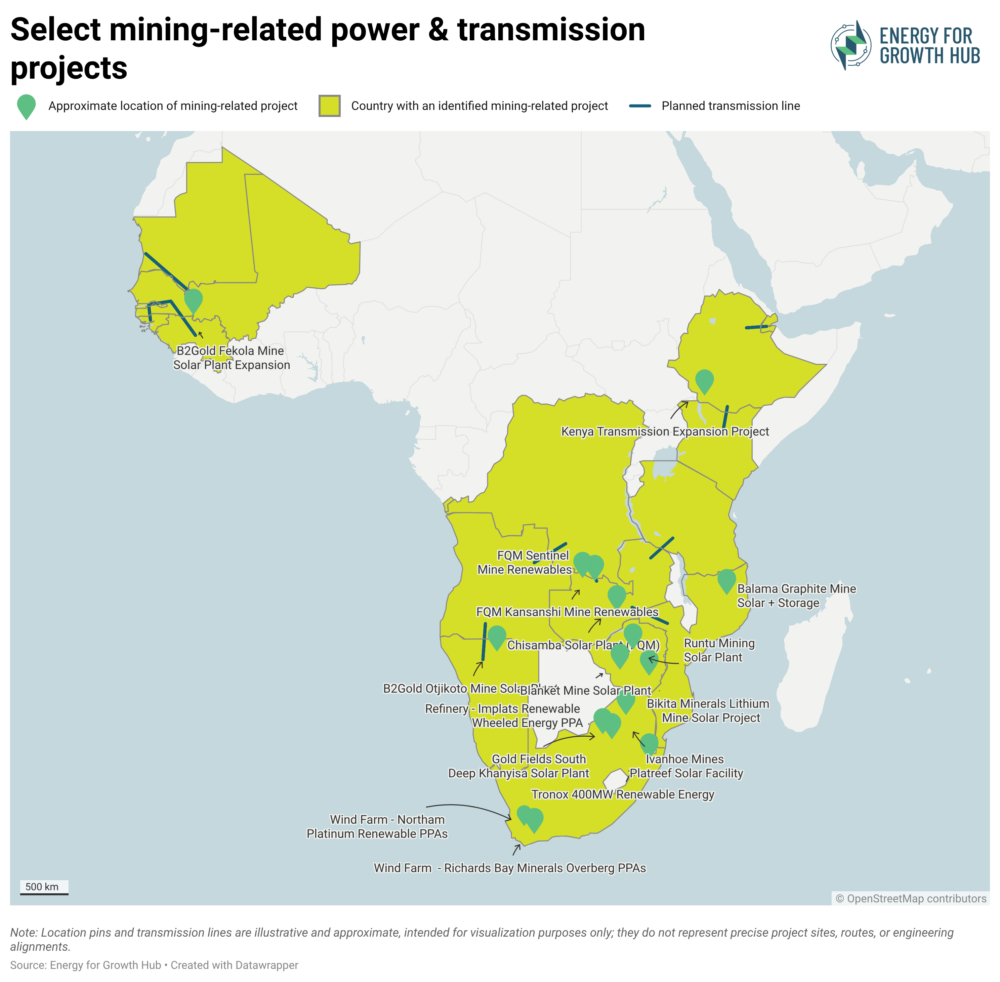

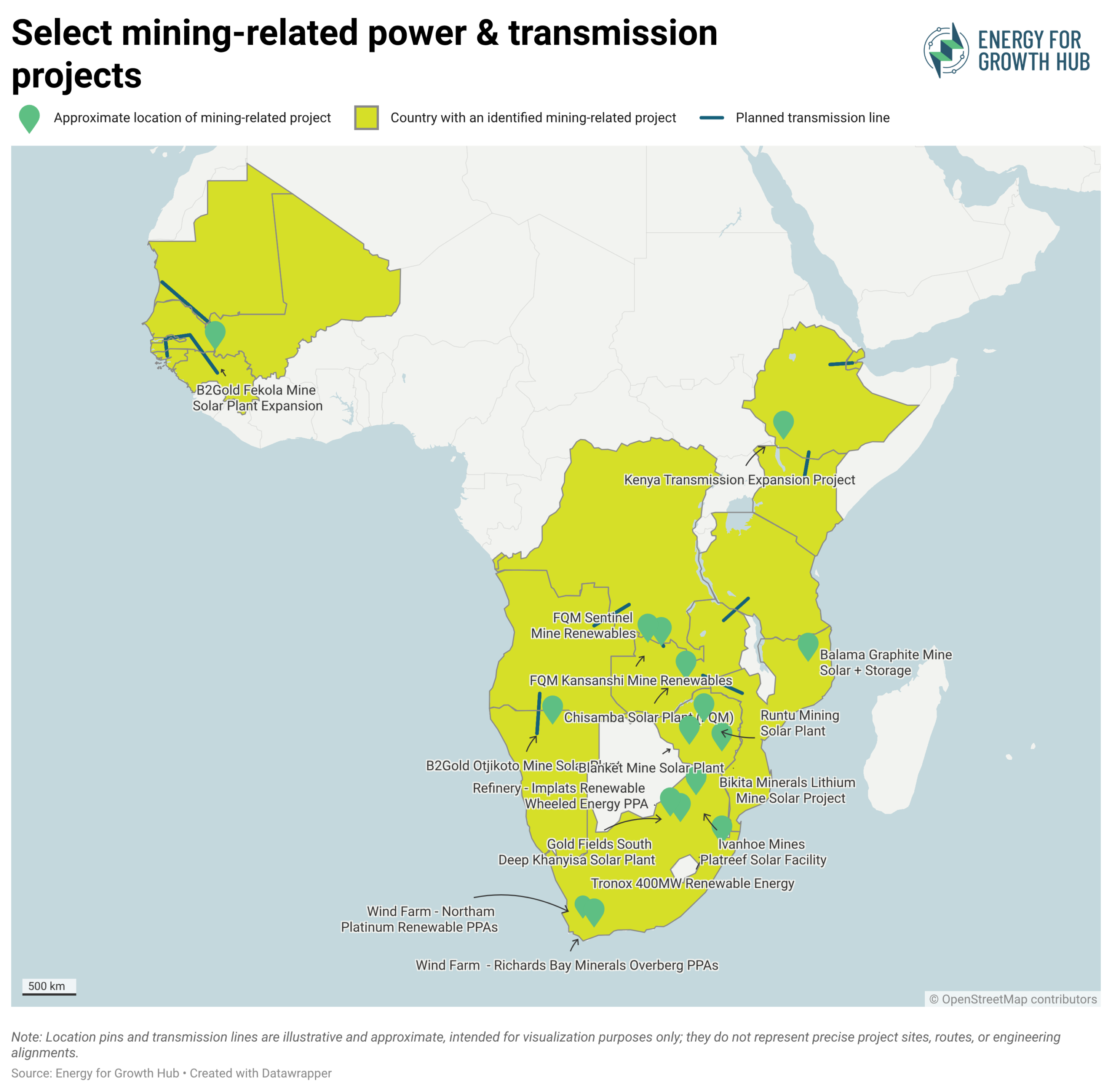

Our approach: We conducted a rapid scan of 25 public, mining-related energy projects, both planned and recently commissioned, through November 2025, identifying projects across 10 African countries. This is not exhaustive; it represents what we could find through public announcements and press releases, but the patterns are instructive for understanding how the sector is navigating power challenges.

Here are the major trends we found in the announcements:

- Mining companies are pursuing both captive power and grid-based solutions. Of the 15 generation projects, eight were captive (self-owned and self-used by mining companies), and seven were grid-connected. And 10 were planned transmission projects connecting mines to regional grids. Three of these transmission projects are explicitly using guaranteed long-term demand from the mines to make infrastructure investments financially viable. This shows mining companies are pursuing both on-site independence and grid-based solutions.

- Low-cost renewables and cross-border electricity dominated investments. Almost all generation projects were solar PV, with three even pairing with battery storage. A majority of the planned transmission projects connect power export from hydro-rich but low-local demand countries like Ethiopia, Tanzania, Mozambique, DRC, or Angola to mining activities across southern Africa. Near or far, low-cost renewables are powering mining activity in Africa.

- The scale of grid-connected generation to supply mining surpasses expectations. Purely captive installations tended to range from 5-52 MW. The grid-connected generation projects that some mining companies are developing were 100 MW or greater. In Zambia, First Quantum alone is developing two projects totaling 430 MW, more than what the country added to its entire grid between 2021 and 2023. This suggests mines are building permanent power infrastructure, not just temporary emergency backup.

But, policy response to these trends has been inadequate:

- Mining is anchoring power investments, and policy must extend its impact. Mining companies are investing in large-scale generation and anchoring long-term energy offtake agreements for transmission infrastructure. With rising demand for African minerals, this dynamic will intensify. Policymakers must strategically use these demand centers and ensure national and regional growth plan alignment to extend benefits beyond the mine fence and the pocketbook of select companies.

- Grid defection is not inevitable or binary → utilities can win back their largest consumers. Rather than fully defecting, companies are investing in both self-generation and grid connectivity to hedge against unreliable or unavailable supply. This creates an opportunity: utilities that improve reliability can retain high-load, creditworthy customers like mining operators — while helping firms avoid the cost of duplicative, self-supplied power systems.

- Regional transmission and power exports: duplicative or strategic? Almost all of the cross-border transmission projects target southern Africa’s mining sector as a key offtaker. This is happening as mining operators continue to acquire self-generation, countries like Zambia rush to sign lots of power deals to increase local power supply, and Mozambique is likely to have excess power from a large smelting closure. It’s unclear whether these regional exports are a coordinated response to a clear demand call or if countries are competing for the same few sets of large industrial consumers. Policymakers, utilities, and development financiers need to take a regional view and ask the hard questions about demand, timing, and trade-offs.

Mining energy demand in Africa is large, but the response is falling short due to limited information. If our rapid, limited scan of recent project announcements is any indicator, the scale of power demand for the mining sector is large; the unmet demand is likely larger. In response, mining companies are developing parallel on- and off-grid power systems, while governments are pursuing costly regional transmission projects to secure the few key demand centers. Yet all of this is unfolding with limited publicly available information on how mines are powered, whether they are grid-connected, their tariff arrangements, on-site generation capacity, or how demand would evolve under reliable supply. Operating under this major blind spot, utilities and decision makers are missing key investment opportunities and pursuing incomplete solutions.