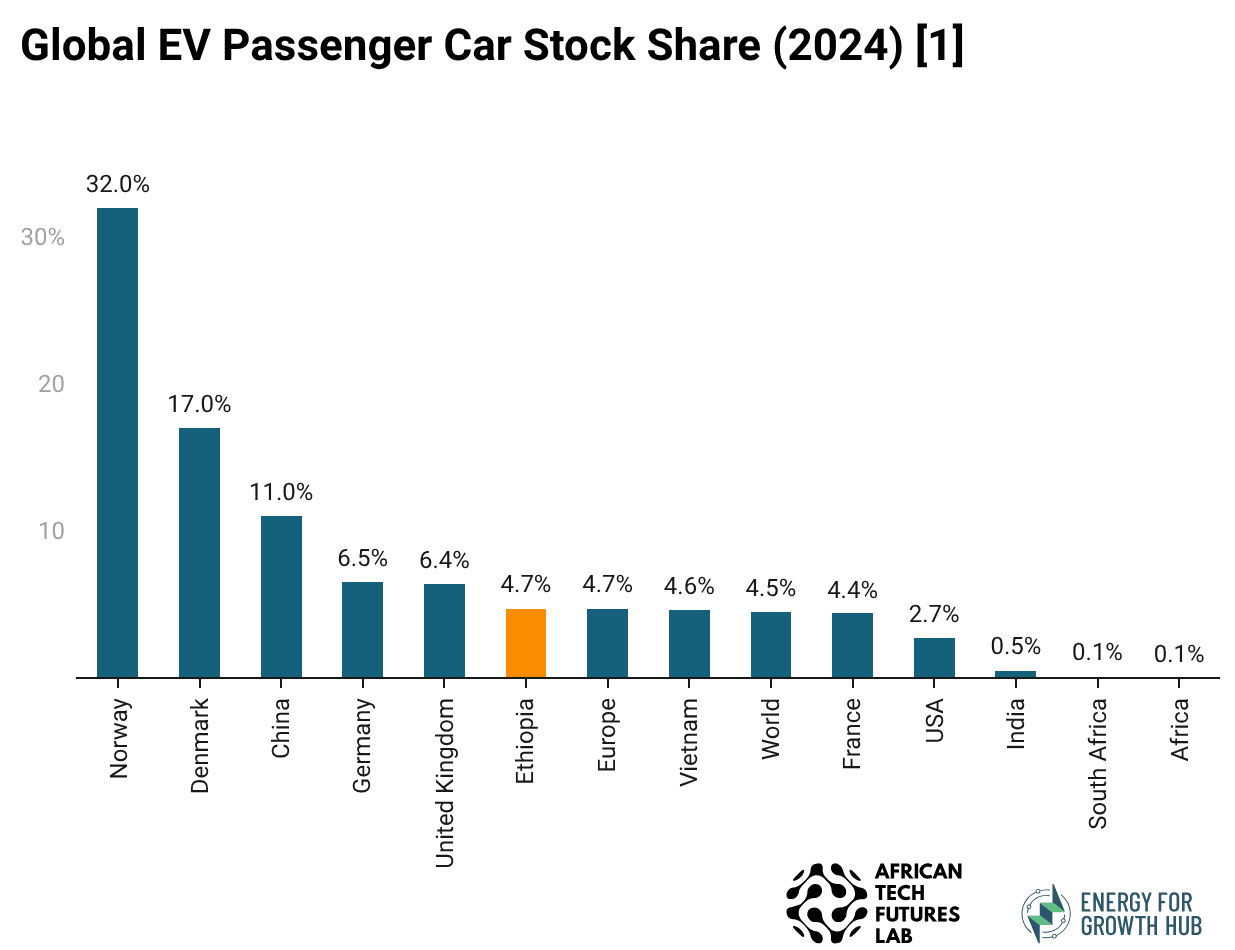

In our previous analysis, we reported Ethiopia’s startling pivot from one of Africa’s least motorized countries to the continent’s most electrified vehicle market. New disaggregated data on passenger car stocks now allows us to place Ethiopia’s progress in a global context. The result is remarkable: by EV passenger car penetration, Ethiopia is not only first in Africa, but ranks alongside global leaders.

Nearly 5% of cars in Ethiopia are electric, at pace with both the global and European averages, and ahead of countries like the United States (2.7%) and India (0.5%). Within Africa, Ethiopia is a clear outlier. Its roughly 15,000 EV passenger cars represent more than four times the stock in South Africa, the continent’s largest auto market, which has an estimated 3,500 EV passenger cars.

This is an extraordinary outcome for one of the world’s poorest and least motorized countries, driven in large part by an aggressive EV policy push, including the world’s first ban of internal combustion engine (ICE) vehicle imports. However, Ethiopia’s recent EV successes must be interpreted with caution. Maintaining momentum will require affordable and reliable electricity, expanded charging infrastructure, improved access to financing, sustained macroeconomic stabilization, and credible data systems to track progress.

Enablers of EV Growth in Ethiopia

- Aggressive pro-EV policy: Two years since enacting the ICE ban in January 2024, EV adoption has grown from less than 1% to nearly 6% of all vehicles on the road. The ban is also reinforced by low customs duties and other tax incentives for EVs. At the same time, ongoing fuel subsidy reforms have tripled pump prices amid a history of chronic fuel shortages, further strengthening the economic case for EVs. The current fuel crisis stemming from the Iran war will likely intensify this trend. Locally assembled EVs also benefit from significant duty reductions and tax exemptions, and 17 EV assembly plants are now operational, with a government target of 60 by 2030. Ethiopia has also set ambitious targets of 148,000 EVs by 2030, alongside plans to install charging stations every 50 to 120 km across every major highway.

- Legacy of a distorted ICE vehicle market: Like most African countries, Ethiopia’s roads are dominated by used ICE cars, which accounted for 85% of vehicle imports in 2023, the year before the ICE import ban was imposed. But unlike many peers, Ethiopia’s automotive market has been heavily constrained by extremely high import duties — historically as high as 200% — combined with chronic foreign currency shortages, which have long made car ownership out of reach for most Ethiopians. This structural mismatch between demand and access even gave rise to a rare phenomenon where used cars in Ethiopia often appreciated in value, highlighting the depth of market scarcity. The rapid EV growth we are now observing is partly a rebound effect. The new EV-led policy regime, alongside broader macroeconomic reforms including an overhaul of its foreign exchange system, has helped resolve some of these longstanding distortions and release pent-up demand.

- GERD coming online: As the Grand Ethiopian Renaissance Dam (GERD) finally comes online, it could ease long-term electricity supply constraints and strengthen the foundation of Ethiopia’s EV transition. With a maximum capacity of 5,150 MW, GERD is expected to roughly double Ethiopia’s current electricity output, in a system where 97% of electricity already comes from hydropower. However, the mere increase of generation capacity does not guarantee reliable power needed to underpin the growth of energy demand centers such as EVs, which requires sustained investments in downstream grid infrastructure.

- Chinese EVs and Chinese-backed EV startups: The influx of low-cost Chinese EVs has reshaped Ethiopia’s automotive industry. Chinese firms are not only exporting vehicles to Ethiopia, but are also embedding themselves across the EV ecosystem, from financing to local manufacturing. For example, BYD has partnered with local credit company Mobilit-E to offer financing for their vehicles, and with Addis-based retailer Moenco to supply EV parts and establish a manufacturing plant in Ethiopia. Local EV company Belayneh Kindie Motors assembles minibuses and buses using components from China’s Golden Dragon Company, while local car importer Tamrin Motors partnered with China’s JAC Motors to introduce affordable EVs in Ethiopia through import and local assembly. This pattern is likely to deepen as Chinese manufacturers consolidate their dominance across the global EV value chain and continue expanding into emerging markets where cost competitiveness and policy alignment create favorable entry points.

Constraints to EV Growth in Ethiopia

- Concentrated in Addis: Nearly all EVs remain concentrated in the capital, which also makes up 95% of all new car registrations. Most charging stations are also located in the capital, making EV ownership highly impractical elsewhere. This concentration also reflects Ethiopia’s broader urban-rural electricity divide. Only 55% of the population has access to electricity, with a large gap between urban access (95%) and rural access (44%). As a result, EV adoption remains primarily an urban phenomenon.

- Limited charging infrastructure: According to public data, Ethiopia has only 13 public charging stations. The Ethiopian State Minister of Transport and Logistics recently cited a figure of 500 EV chargers, mostly in Addis, but no official report confirms total or private charging numbers.

- Extremely low motorization rate: Even in comparison to low-income countries, Ethiopia has one of the lowest car ownership rates: 6.7 vehicles per 1,000 people compared to the Africa-wide average of 73 in 2016. Ethiopia’s motorization rate climbed only modestly to 11.2 per 1,000 people in 2022.[2] Low income levels and historically restrictive automotive policies have kept motorization rates extremely low. With a GNI per capita of $1,100, Ethiopia trails regional peers like Kenya and Ghana with per capita incomes almost twice as high and significantly larger vehicle fleets. This pattern is consistent with our analysis, which shows a strong correlation between income levels and motorization rates both regionally and globally.

- Limited access to financing: Electric vehicles remain expensive, with few models priced below $11,000 (1.7 million birr). However, in addition to income constraints, access to financing remains extremely limited, further affecting affordability. Only 5% of Ethiopian adults have borrowed from a formal financial institution or used a mobile money account, compared to 12.6% across Africa and 40% in Kenya. Growth of Ethiopia’s EV market will ultimately be constrained by this overall income and affordability challenge, requiring broad-based economic development in addition to tackling EV-specific barriers.

- Unreliable electricity: Though electricity in Ethiopia costs about $0.10 per kWh, roughly half of that of neighboring countries, and significantly less than the US average of $0.18 per kWh, unreliable supply and frequent power outages remain a major constraint to the growth of energy demand centers across its economy, including EVs.

- Significant gaps in EV market data: Data on EV adoption across Africa is deeply fragmented, inconsistently reported, and rarely verified, and Ethiopia is no exception. For example, figures from the Ministry of Transport estimate around 100,000 EVs across all vehicle segments, while the 2024 U.S. International Trade Administration (ITA) Ethiopia EV market analysis estimates the number may be closer to 30,000. Disaggregated vehicle data is also scarce: Ethiopia’s latest energy outlook report specifies the number of EV passenger cars but doesn’t share data on other vehicle segments like buses, trucks, or two-wheelers. Meanwhile, global EV market trackers from organizations such as the IEA and BloombergNEF continue to overlook the continent beyond a few countries like South Africa. In the absence of reliable, comprehensive data, it is difficult to capture actual market trends accurately and guide effective policy and investment.

Conclusion

Ethiopia’s EV penetration story remains astonishing: a low-income, low-motorized country outpacing much of the world. This is a rare success story that demonstrates what aggressive policy interventions can achieve. However, the credibility and long-term sustainability of Ethiopia’s EV progress will depend on addressing electricity access and reliability concerns, infrastructure constraints, affordability issues, and data gaps. If Ethiopia addresses these challenges, it could offer a sustainable model for EV adoption in other developing markets.

Endnotes

- We define “EV passenger car stock share” as the proportion of electric passenger cars relative to the total number of registered passenger cars in each country. Electric (15,000) and registered (320,000) car data for Ethiopia is sourced from the Ethiopian Energy Outlook 2025. Data for all other countries is from IEA’s Global EV Data Explorer. Both Ethiopia and IEA data is for 2024.

- We calculate Ethiopia’s latest motorization rate by dividing the total number of registered vehicles in 2022 (Ethiopian Energy Outlook, 2025) with the total population in 2022 (World Bank).