Higher prices for oil & gas should be good news for wind & solar energy and drive an even faster energy transition – at least in rich countries. Outside of mature markets, the story could be different, because soaring inflation and an increasingly risky global economy are driving up risk premiums, which will undercut clean power development.

Renewables are especially CapEx-heavy…

Every source of clean power – wind, solar, hydro, geothermal, and nuclear – is heavily weighted toward initial capital expenditure, meaning that their costs are highly sensitive to increased interest rates. Most of the costs of a solar plant are for the panels and other infrastructure, while most of the cost of a gas-fired power plant is in the fuel rather than the plant itself. Fuel costs are determined and paid for at the time of use, while upfront capital costs must be financed and paid on a schedule regardless of use. Here’s an illustrative example of the estimated cost impacts of unsubsidized financing on three different types of energy projects in two very different interest rate environments:

| LCOE (US$/kWh) | US | Ghana |

|---|---|---|

| Solar PV w/ Single Axis Tracking + Battery Storage | $0.12 | $0.29 |

| Solar PV w/ Single Axis Tracking | $0.09 | $0.21 |

| Combined-Cycle 2x2x1 | $0.09 | $0.12 |

Source: Author estimates using the NREL calculator

Higher borrowing rates (for loans) or hurdle rates (for equity) imply only modest increases for less CapEx-heavy energy sources like gas or coal, but suggest huge cost increases in the LCOE of energy sources with significant upfront costs. Unsubsidized solar costs ~140% more in Ghana than in the US solely because of differentials in cost of capital.

…And the problem is getting worse for African markets

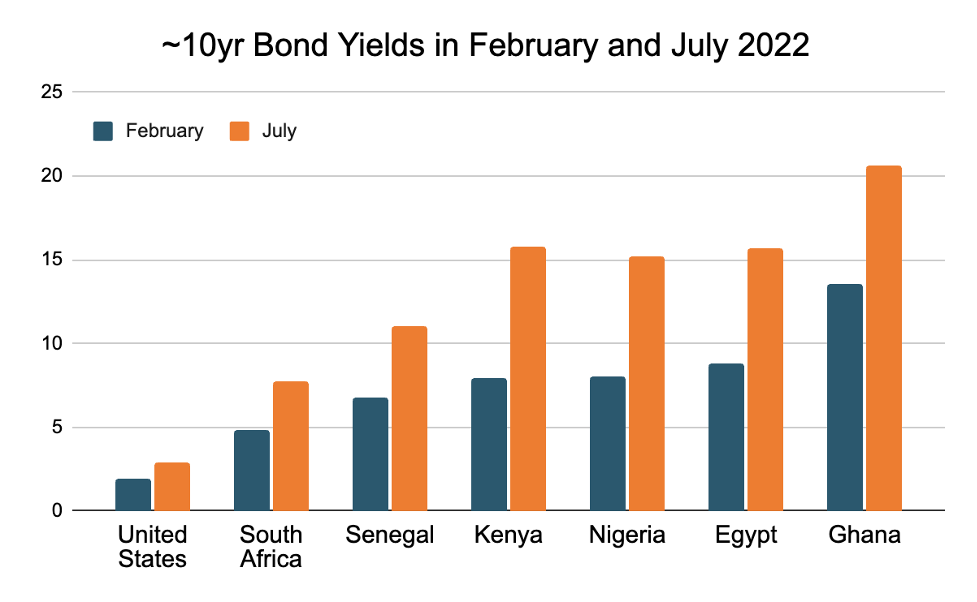

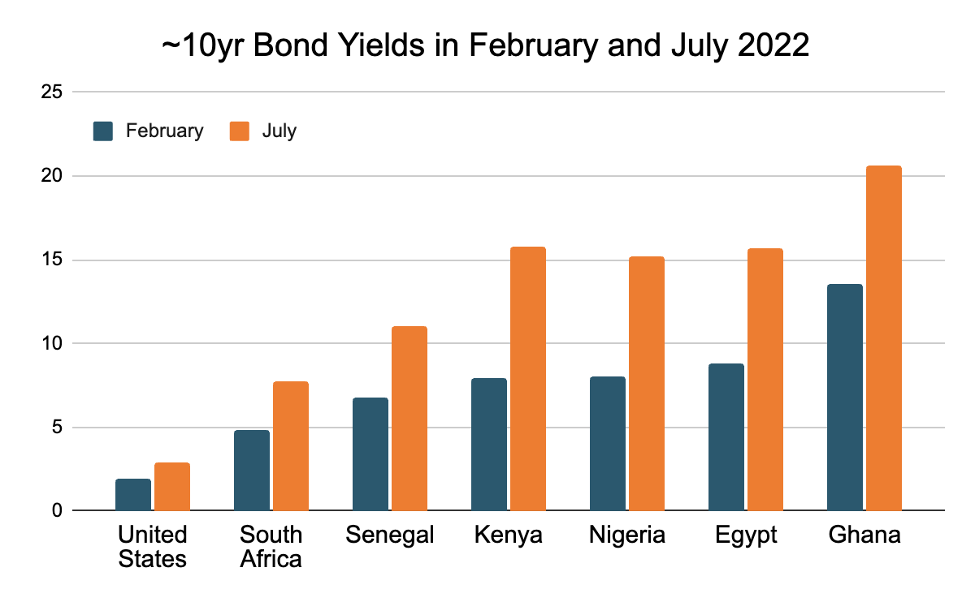

Investments in emerging markets already faced far higher borrowing rates in a relatively stable global economy. In just the last 6 months, the average Country Risk Premium for African nations has risen more than 500 basis points, doubling since February 2022. The yield on 10-yr dollar-denominated sovereign bonds is a useful proxy for investor confidence in a given economy.

Source: J.P. Morgan ESG EMBI Global Diversified Index

Bottom Line: The headwinds for clean energy are getting stronger

An uncertain international economy is hitting renewable energy hard. We can’t simply assume historic deployment rates will continue, especially in emerging economies in Africa and other high-interest rate environments – where the majority of future energy demand growth will occur. If wealthier nations expect poorer ones to deploy CapEx heavy clean energy, they need to be prepared to drive down borrowing costs for projects in these markets.