Ghana’s rapid population growth and ambitious development agenda will significantly increase electricity demand. The government has developed various strategic plans in response. Understanding both the current and potential pathways is crucial to Ghana’s next policy making steps.

Current Energy Resources in Ghana

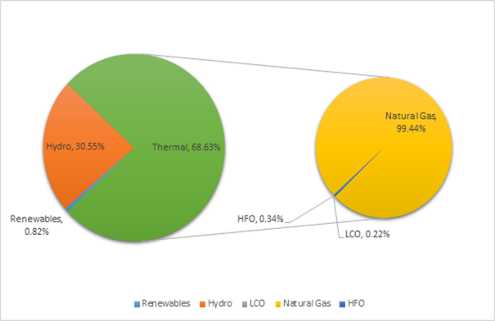

According to Ghana’s Energy Commission, final energy consumption increased by 4.3% in 2019. Peak electricity demand for 2019 was 2804 MW, well under Ghana’s total installed capacity of 5,172 MW. Installed capacity is dominated by thermal (68%), followed by hydro (31%), and marginal renewables (0.82%)(Figure 1). Ghana’s thermal dependency is due to high demand, unpredictable water levels in domestic dams, discovery of indigenous oil and gas, and the introduction of the West African Gas Pipeline.

- Domestic: The country’s domestic resources comprise crude oil, natural gas, hydropower, and non-hydro renewable energy (solar, wind and biomass).1

- First discovered in 2007, Ghana’s commercial quantities of crude oil are an estimated 1,019 million barrels, which is entirely exported.2

- Some oil discoveries (Jubilee and TEN fields) have natural gas deposits. Combined with other discoveries like Offshore Cape Three Points, gas reserves totaled around 1,936 billion cubic feet in November 2019, used entirely in-country.3

- Imports: Ghana imports natural gas from Nigeria through the West African Gas Pipeline and electricity from Côte d’Ivoire when there are disruptions in local generation. The Tema LNG terminal project (scheduled to be completed 2021) will give Ghana access to global gas markets as well.

FIGURE 1: Installed power capacity mix in 2019

What does the Integrated Power Sector Master Plan (IPSMP) project for Ghana’s future energy mix?

The 2019 IPSMP projects possible demand and supply dynamics through 2030:

- Generation and Demand. No additional thermal capacity will be needed until the mid-2020s due to the gas-fired plants already under construction or recently commissioned, which will add a dispatchable capacity of 936 MW.

- Indigenous resources (hydropower, renewables, and natural gas) are the least-cost option over the entire planning period to improve energy security, and allow gradual grid integration of solar and wind.

- Renewable Energy. Ghana has a goal of 10% renewable generation by 2030. In the IPSMP reference case scenario, the country will add a total of 520 MW of solar, 325 MW of wind and 60 MW of hydro from 2022 – 2030.

- Nuclear. If the government decides to develop nuclear capacity by the early 2030s, it will likely need to defer some planned gas power to avoid overgeneration. Nuclear plants generally cost more to build and require more regulatory oversight, but have lower operational costs and are less prone to market fluctuations than coal or gas.

- If gas prices fall and Ghana can produce or procure ample supply, gas will remain the least cost option for baseload and dispatchable power, and nuclear development may be delayed or canceled.

- If Ghana’s gas supplies are depleted or demand rises faster than imports, then nuclear power will be an attractive option into the 2030s and 2040s.

- Ghana may explore lower cost and easier to build Small Modular Reactors as direct replacements for gas plants as they retire or resources deplete.

What can Ghana do to achieve its energy mix goals?

- Refine the target for 10% renewable energy by 2030. Ghana’s current generation mix is near 40% low-carbon, with 39% hydro and 0.5% solar. However, the Renewable Act (832) did not originally consider hydro projects over 100 MW — including Akosombo (1020 MW), Bui (400) or Kpone (160) — as renewable. The government later amended the act to include large hydro, meaning Ghana has already met its 2030 goal and should realign its target to be more ambitious.

- Revise the legal provisions that block renewable energy development. The Renewable Energy Master Plan calls for $460 million of investment in renewables annually from 2019 – 2030, with 80% coming from the private sector. But two well-intended existing laws may inhibit private investment:

- The government’s moratorium on new generation investments due to overcapacity. There is no specific timeline as to when the moratorium will be lifted.

- Local Content Regulations (L.I. 2354) require compulsory partnerships with Ghanaian businesses and funding from Ghanaian banks. But the Association of Ghana Industries cites access to credit and high interest rates as two of the top five challenges businesses face, potentially hindering project development.Both the moratorium and the local content provisions need to be revised to enable more investment in renewables.

- Develop natural gas generation that complements renewables. Ghana will need additional gas-fired combined cycle capacity beyond the 2020s. As the country harnesses more gas, it should plan long-term to ensure new plants complement renewable power. Three factors make natural gas a good fuel for firm power:

- Availability. Ghana currently has three fields that produce natural gas, is under contract for imports from Nigeria, and developed a 250 mmscfd capacity regasification facility with the national oil company.

- Cost. Natural gas is cheaper than heavy fuel oil (HFO). Exactly how much natural gas will be used will depend on gas pricing, availability, environmental commitments, demand and existing national plans.

- Climate ambitions. Ghana’s Nationally Determined Contribution under the Paris Agreement highlights energy as a core focus, with targets that include natural gas as key for emissions reductions.

What factors may impact the IPSMP’s success?

Ghana’s previous long-term energy plan, the Strategic National Energy Plan (2006-2020), was not successfully implemented, leading to power crises. The drafting of the IPSMP was more inclusive of interested parties, used a more robust methodology, and received support from partners like the World Bank and USAID. The improved planning process has made the IPSMP a key policy reference point, and its demand projections are likely accurate since it considers scenarios including climate commitments, natural disasters, historical trends, and social, geographic and economic conditions. However, two market drivers may affect its projections’ accuracy:

- Increased demand for distributed energy systems and self generation can pose challenges to existing investments in generation, transmission and distribution if not properly managed. Some energy-intensive companies such as Kasapreko Company Limited and Unilever have invested in distributed solar, and in areas like Prestea and Tarkwa, some mining companies have contracted Genser to build and operate gas-fired captive plants for the mines. Grid defections from industrial customers impact demand projections.

- Increased export to countries such as Burkina Faso and Togo means that Ghana will require more capacity, which will have to guarantee affordability and reliability in order to compete against countries like Nigeria that can offer low gas prices.

With these factors in mind, the government should commit to periodic review of the plan’s projections and implement a procurement policy that ensures all new capacity is contracted by open, transparent and competitive tendering in line with the IPSMP to enhance affordability and accountability.

Endnotes

- Act 832 (Renewable Energy Act) does not recognize large hydro as a renewable energy source.

- Energy Commission, District Energy Profile

- Energy Commission, District Energy Profile