High power generation costs in Sub-Saharan Africa are driven by stark imbalances in supply and demand, poor utility performance, and constraints on independent power producers. These make cost recovery difficult and block execution of new projects. Regional power trading can help.

Africa’s power pools can help balance supply and demand

Only 3%

of power generation from WAPP member utilities crosses borders1

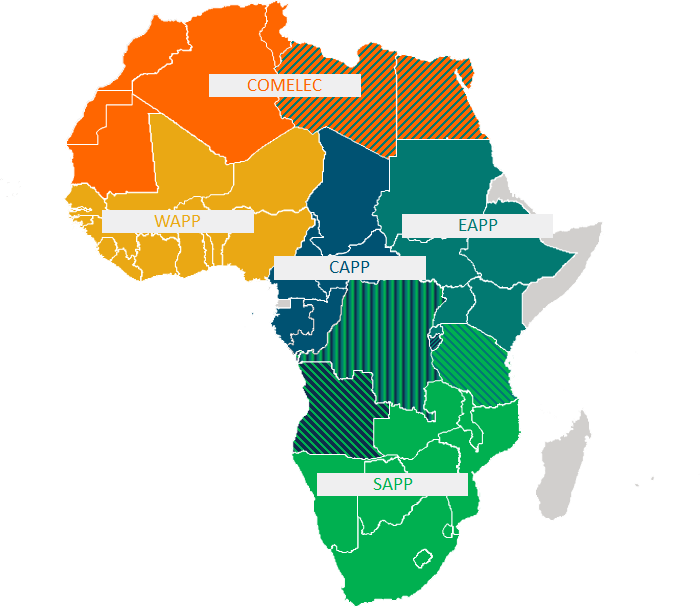

- The continent has five regional power pools. [See Table 1 and Figure 1]. Electricity shortages and surpluses destabilize country-level electricity markets, constraining advancements that support economic growth.The majority of Sub-Saharan countries face power supply deficits, but some actually face overgeneration issues (and the resulting risks to utility fiscal health) in the short to medium term.1

- Private generation boomed in the region from 1995-2015, with IPP capacity doubling every five years in that period, but the requisite investment in transmission and distribution did not occur.2

- If generation buildout continues as planned, Ethiopia, Kenya, Tanzania, Uganda, and Rwanda could face regional overcapacity of 2,689 MW by 2022.3 Without needed transmission and distribution infrastructure upgrades to reach new customers or markets, existing overgeneration will not reach paying customers, and new projects will face serious off-taker risks.

- In Kenya, overgeneration is already stalling renewable energy projects.4 Kenya Power recently froze new PPAs, impacting over 900 MW of pre-contracted PV capacity. The move also reduces contract security for more mature projects already weathering tariff renegotiations.5

Benefits of regional power trading

$5-8 billion

USD est. annual generation and transmission cost savings in WAPP6

- Significant savings in capital and operating costs. Shared infrastructure, financial transparency, and natural incentives for efficiency drive down CAPEX and OPEX costs for electrical infrastructure, with massive potential for savings. Estimates suggest the Southern African Power Pool (SAPP) members could save $42 billion on capital investment and O&M costs with full market and technical integration, while the World Bank estimates that the West African Power Pool (WAPP) members could save $5-8 billion per year in generation and transmission costs, as well as cut retail rates and outage hours by about half.6,7,8

- Improved utility operational performance. Utilities can import and export power to mitigate overgeneration and curtailment, as well as support ramping and other grid balancing needs. Reliability of service and resiliency of supply are also bolstered by reserve sharing.9

- Enhanced bankability for new IPP projects, particularly intermittent renewables. Most national grids in Sub-Saharan markets could only host a few hundred MWs of intermittent renewable energy, but regional power trading allows IPPs to site projects in one country and contract power to meet demand from public or private entities in another, reducing off-taker risk and curtailment risk, among others.10 In the short term, cross-border trading also improves IPP bankability by allowing arbitrage of price differentials.

- Increased regional cooperation. Coordinated planning of critical infrastructure requires political cooperation, and creates economic dependencies which promote trade and peace.11,12

Challenges to improved regional power trading in Africa

- Bundled utility markets. Liberalized power markets would permit IPPs, distribution companies, and even large corporate offtakers to trade directly in the power pool, rather than just single-buyer or incumbent utilities.13

- Regulatory incompatibility. Without regulatory harmonization, buyers and sellers may face uneven market constraints that could imbalance power flows. Rulemaking for interconnection, access, contract terms, dispute resolution, tariff-setting, and wheeling charges across differing legal frameworks can be stifling.14

- Proving bankability. Aggregating the creditworthiness of multiple utilities is complicated by offtakers across borders with different (often not cost-reflective) regulatory regimes.15

Technical integration and balancing. Successful integration requires significant investment in transmission and distribution infrastructure that would allow for cross-border trade. If investment in capacity stagnates it would severely limit the benefits of regional integration. - Over-reliance on anchors. Power pools with one large market of excess generation or load shortfalls may need to balance disproportionate influence on transmission planning or rulemaking.

Bottom Line: Quickly and effectively developing Africa’s regional power pools could help match surpluses and shortages and improve access to grid-scale energy, utility performance, and large-scale solar PV bankability for independent power producers.

Table 1: Africa’s Regional Power Pools16,17

| POWER POOL | MEMBER COUNTRIES |

|---|---|

| The Southern African Power Pool (SAPP) | Established in 1995 by 12 Southern African Development Community (SADC) countries, the SAPP is by far the most advanced electricity market on the continent, with daily and hourly contracts and competitive day-ahead markets in place since 2003. Nine of the twelve SAPP member countries are currently interconnected; Angola, Malawi, and Tanzania are expected to be interconnected by 2021. |

| The East African Power Pool (EAPP) | Though it was legally established in 2005, the EAPP only began power trading in 2018. EAPP is moderately integrated to the SAPP through the Zambia-Tanzania-Kenya interconnection, but is facing power surpluses due to overgeneration if sub-regional transmission planning is not improved. |

| The West African Power Pool (WAPP) | Established in 2000 by the 14 countries of the Economic Community of West African States (ECOWAS) countries, is in the midst of launching its regional grid interconnection effort, and plans full completion of cross-border grid linkages planned by 2020. |

| The Central African Power Pool (CAPP) or Pool Energétique d’Afrique Centrale (PEAC) | Established in 2003 by 11 Economic Community of Central African States (ECCAS) countries, has very limited power trading to date, due to low demand, a weak legal framework, and poor transmission infrastructure. |

| The Maghreb Electricity Committee (COMELEC) | Contains the countries of North Africa and is connected to the Middle East through the Egypt-Jordan connector and to Europe through the Morocco-Spain line. COMELEC states have by far the best electricity access rates, grid infrastructure, and generation capacity, but the market and bulk trading structures are still basic. |

Figure 1: Africa’s Regional Power Pools and their Members

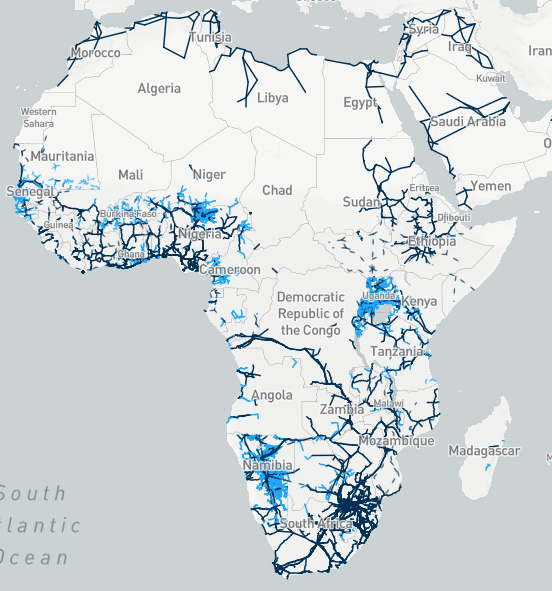

Figure 2: Africa’s Existing and Planned Low, Medium, and High Voltage Transmission Lines18

Endnotes

- Tony Blair (2018). Uniting Africa for Power.

- “Brighter Africa: The growth potential of the sub-Saharan electricity sector,” McKinsey and Company.

- Power Africa (2018). East African Countries Will Have Electricity They Cannot Use, Unless They Focus on Their Transmission Infrastructure Now.

- Rose Mutiso and Jay Taneja (2018). The Seven Major Threats to Kenya’s Power Sector.

- Brian Ngugi (2018). Kenya Power Freeze Puts New Energy Plant Billions on the Line.

- ESI Africa (2018). Power pool plan to maximise energy trade within SADC

- World Bank (2018). Regional Power Trade in West Africa Offers Promise of Affordable, Reliable Electricity.

- This is partially driven by the high share of retail tariffs comprised of T&D charges in West Africa.

- P. Niyimbona (2005). The Challenges of Operationalizing Power Pools in Africa.

- ESI Africa (2019). Insights into challenges surrounding energy projects in Africa

- Trotter, et al. (2018). Solar energy’s potential to mitigate political risks: The case of an optimised Africa-wide network

- Castalia Strategic Advisors (2009). International Experience with Cross-border Power Trading.

- Infrastructure Consortium for Africa (2016). Updated Regional Power Status in Africa’s Power Pools.

- P. Niyimbona (2005). The Challenges of Operationalizing Power Pools in Africa.

- Power Africa (2018). Transmission Roadmap to 2030: A Practical Approach to Unlocking Electricity Trade.

- Callixte Kambanda (2013). Power Trade in Africa and the Role of Power Pools.

- Power Africa (2018). East African Countries Will Have Electricity They Cannot Use, Unless They Focus on Their Transmission Infrastructure Now.

- World Bank Group (2017). Africa Electricity Grids Explorer.