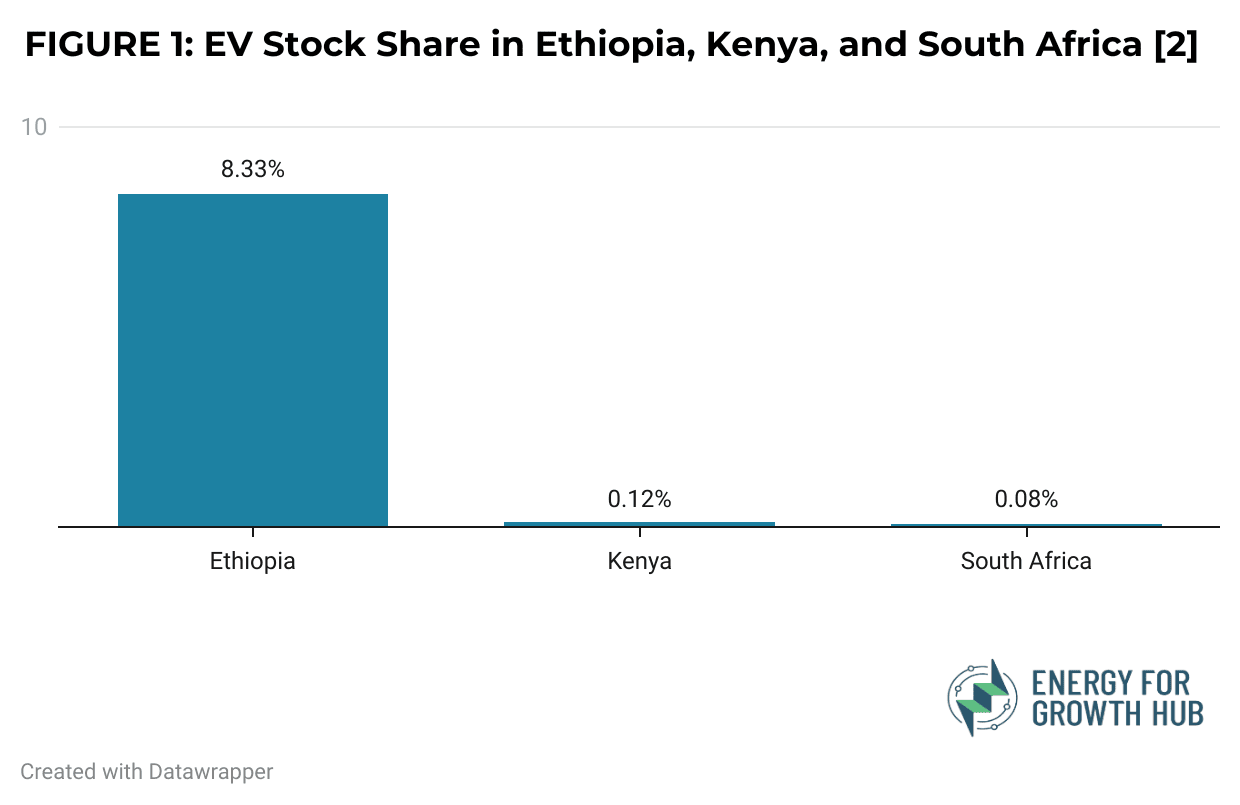

Ethiopia has emerged as an unexpected leader in Africa’s electric vehicle (EV) transition. In 2023, the country became the first in the world to ban imports of internal combustion engine (ICE) vehicles. According to the Ministry of Transport and Logistics, the country now has 100,000 EVs on its roads, accounting for roughly 8.3% of its estimated 1.2 million registered vehicles. If accurate, that would make Ethiopia the clear front-runner in EV penetration on the continent, and a surprising contender among top global adopters [1].

From automotive laggard to EV trailblazer

But Ethiopia’s EV story begins in an unlikely place. Ethiopia has long had one of the lowest motorization rates in Africa — just 6.7 vehicles per 1,000 people in 2016, compared to a continental average of 72.7. This reflects Ethiopia’s low income levels and restrictive automotive policies. With a GNI per capita of under $1,000, Ethiopia trails regional peers like Kenya and Nigeria with per capita incomes almost twice as high and far larger fleets. This pattern is consistent with our analysis, which shows a strong correlation between income levels and motorization rates both regionally and globally.

Like most African countries, Ethiopia’s roads are dominated by used cars, which make up around 85% of vehicles. But a complex mix of high import duties — historically as high as 200% — and chronic foreign currency shortages have long made car ownership out of reach for most Ethiopians. This mismatch between demand and access even gave rise to a rare phenomenon where used cars in Ethiopia often appreciated in value, highlighting the depth of market scarcity.

Against this backdrop, Ethiopia’s EV push marks a dramatic pivot. The ICE ban, combined with import duty waivers and tax exemptions for EVs, signals a radical shift in transportation policy. If government-reported EV figures are accurate, they point to a wholesale transformation of the national vehicle fleet in a remarkably short time period. In just a few years, Ethiopia would have gone from one of Africa’s least motorized countries to its most electrified.

Much of this EV activity, however, is concentrated in the capital Addis Ababa. The city’s stop-and-go traffic, shorter commuting distances, and higher rates of wealth concentration have created an ideal environment for EV uptake. Addis also has an electricity access rate of over 90%, significantly higher than the national average, and is undergoing major road and highway upgrades that will improve conditions for motorization more broadly. Generous tax incentives and growing availability of low-cost Chinese EVs have made them increasingly attractive to urban buyers, who, amid chronic fuel shortages and price hikes, are opting for vehicles they can more reliably charge at home.

Can Ethiopia sustain this momentum?

But serious questions remain about the country’s readiness to sustain such a transition. Only 55% of the national population has access to electricity, and the grid suffers from high rates of outages. The entire country currently has just 13 public EV charging stations. Affordability is another barrier. While EVs benefit from lower import taxes, access to financing remains limited. Formal credit is largely concentrated among salaried urban workers who can access employer-backed loans. Only 5% of Ethiopian adults have borrowed from a formal financial institution or used a mobile money account, compared to 12.6% across Africa and 40% in Kenya.

A recent move toward a more market-based foreign exchange system may ease chronic forex shortages, but the shift has also triggered currency devaluation and rising import costs, straining the automotive market further. Meanwhile, the government is also trying to build a local EV manufacturing base, offering generous tax incentives for vehicles assembled in-country. But progress towards this vision has been slow, and the impact remains limited.

Ethiopia is also expanding its electricity generation capacity through major infrastructure investments like the Grand Ethiopian Renaissance Dam (GERD), one of Africa’s largest hydropower projects. As GERD ramps up, EVs could anchor new electricity demand and absorb surplus power.

Can we trust the numbers?

Data on EV adoption across Africa is deeply fragmented, inconsistently reported, and rarely verified. In Ethiopia, ministry officials have privately cited EV figures ranging from 70,000 to 120,000 EVs. Meanwhile, the U.S. International Trade Administration estimates the number may be closer to 30,000. These figures also don’t disaggregate by vehicle class, making it difficult to assess what’s actually on the road.

This dearth of reliable EV data is not unique to Ethiopia. Across Africa, official statistics are sparse and often derived from one-off press releases, outdated records, or paywalled commercial databases. In contrast, mature EV markets like the US and Europe rely on robust, multi-source systems to track vehicle data. These systems are underpinned by dedicated statistical agencies, standardized reporting protocols, and overlapping data from government, industry, and civil society.

Despite growing activity, Africa remains largely invisible from major global EV outlooks. Forecasts and market reports from organizations such as the IEA and BNEF continue to overlook the continent beyond a few countries like South Africa. In the absence of reliable, comprehensive data, Africa’s EV narrative is shaped by anecdotes and media hype around a handful of startups, offering little reliable data to guide effective policy or investment.

Conclusion

Ethiopia’s historic ICE ban has turned it into a test case for what happens when EV ambition outpaces institutional and infrastructural capacity. The scale of transformation implied by official figures and announced ambitions — targeting 400,000 EVs by 2032 — is unprecedented. Yet, despite these challenges, Ethiopia has already defied expectations. The rapid uptake of EVs, especially in urban areas, reflects a unique combination of policy incentives, market pressures, and user adaptation that can tip the balance towards electrification, even in a challenging context.

For Ethiopia, and for Africa more broadly, the next phase of the EV journey depends not just on bold policy ambition or reactive shifts triggered by market constraints, but on confronting the deeper barriers to readiness — from grid reliability and access to finance, to the data systems needed to track and steer progress. Success will come from the steady work of building the foundations that make EV transitions both viable and scalable.

Endnotes

- Ethiopia’s data for EVs and registered vehicles is not disaggregated by class. As a result, direct comparisons with disaggregated global EV penetration data are not possible. However, it is notable that Ethiopia’s estimated overall stock share is higher than passenger vehicle penetration shares in many mature economies.

- We define “EV stock share” as the proportion of electric vehicles relative to the total number of registered vehicles in each country. These data are reported for all vehicles with no disaggregation by vehicle class. Registered vehicle data for Kenya is from CEIC (2022); for Ethiopia from the CCG Transport Data Starter Kit (2020); and for South Africa from the South African Ministry of Transport (2023). EV stock data for Ethiopia is from the Ministry of Transport and Logistics (2024); for Kenya from the Energy and Petroleum Regulatory Authority (2024); and for South Africa from the IEA Global EV Outlook (2024). EV stock shares were calculated by dividing the reported number of EVs by the total number of registered vehicles in each country.