Summary: Governments in emerging gas-producing countries often want to prioritize domestic use, but exports are not always at odds with building downstream consumption at home.

Why it matters: Natural gas is viewed as a critical component of development in gas-producing countries. It is an excellent industrial fuel and necessary feedstock for many chemical processes. In a power generation role, gas is cleaner than coal or diesel and well-suited for providing backup generation to support large build-outs of wind and solar. All of these uses can help drive economic growth and job creation.

LNG exports are easier to finance than domestic (in-country) gas uses

While developing domestic gas consumption is attractive, the high upfront cost of infrastructure to produce and transport natural gas means gas developments require reliable long-term returns in order to attract investors. In countries without mature existing gas markets, exports (often via LNG tankers) tend to offer more predictable returns — and thus prove easier to finance — than projects aimed at supplying domestic gas-using applications, for the following reasons:

- International gas prices are higher. Gas-producing countries, especially lower-income ones, tend to set domestic prices at below-market rates in the interest of affordability.1 This makes international markets more attractive to gas producers. This is particularly true in the current market environment where LNG prices are likely to remain high.

- Domestic customers do not always pay reliably (and it’s not always their fault). Gas-fired power plants are a popular domestic application for gas, but power companies in lower-income countries can fail to pay on time for the gas they use, often because structural problems in the power sector make it hard for them to collect from their own customers.2 The vast majority of African utilities, for example, consistently operate at a loss.

- International financial institutions are more supportive of exports. Multilateral lenders like the World Bank are under pressure from their member countries to limit financing for projects that use fossil fuels, even when such projects have important development benefits.3 However, energy security concerns in wealthy, gas-dependent countries have recently encouraged these institutions to relax constraints on financing gas developments aimed at export, even while in-country uses like gas-fired power continue to face an adverse funding environment.4

But it’s not a zero-sum game: value chains built for LNG exports can help facilitate domestic gas use

The gas development trajectories of lower-middle-income and upper-middle-income countries that currently export LNG (Figures 1 and 2) suggest the following observations:

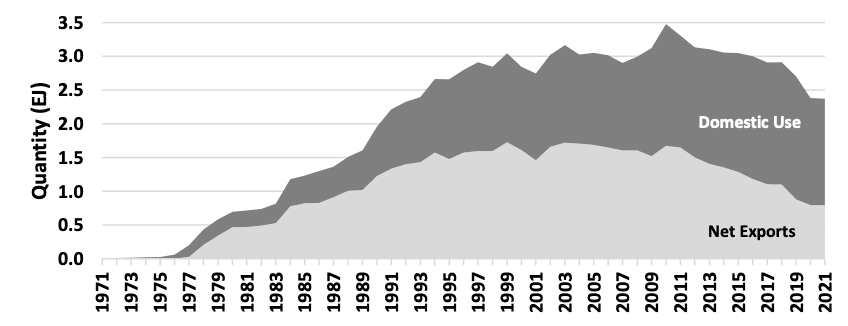

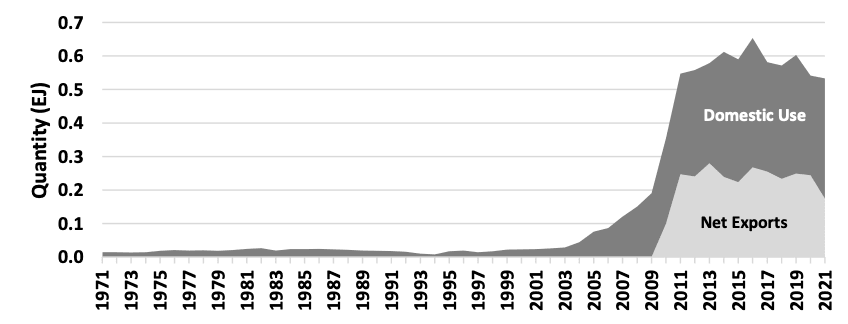

- LNG export projects are linked to increases in gas production. All of the gas development trajectories in Figures 1 and 2 show significant increases in gas production (the sum of “Domestic Use” and “Net Exports”) coinciding with the start of exports. This is because LNG exports allow the entire production-transportation-liquefaction value chain to be financed. For example, financing from the Japanese government for the path-breaking Arun LNG project to export gas to Japan led to the development of Indonesia’s natural gas supply industry (see Figure 1(b)).5

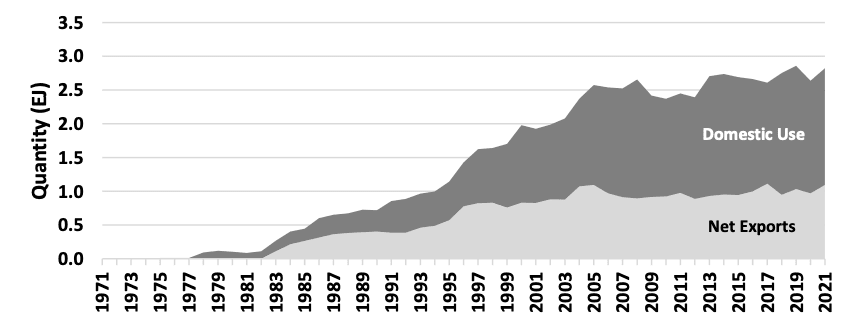

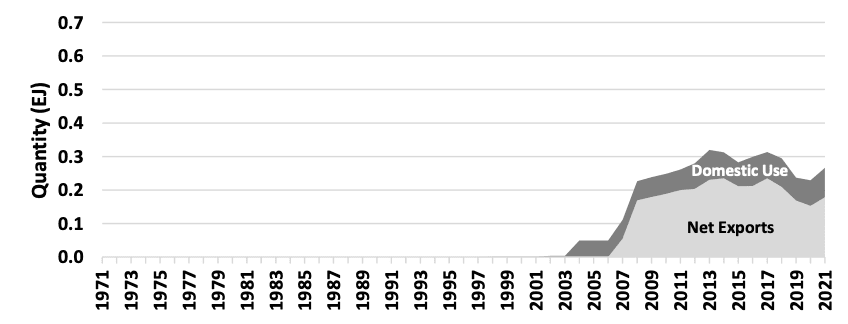

- LNG exports don’t suppress domestic consumption of gas — and can boost it. In all the countries examined here, domestic gas use was as high or higher after the start of LNG exports as it was before. Because gas for LNG exports usually comes from new developments, exports don’t generally cannibalize domestic gas use. When export markets spur the development of a significant gas field, as with the Camisea field in Peru, there can be a step jump in both domestic use and exports (Figure 2(d)). In Indonesia and Malaysia, domestic use of gas rose steadily as export quantities grew in the two decades following the start of LNG exports (Figures 1(b) and 1(c)).

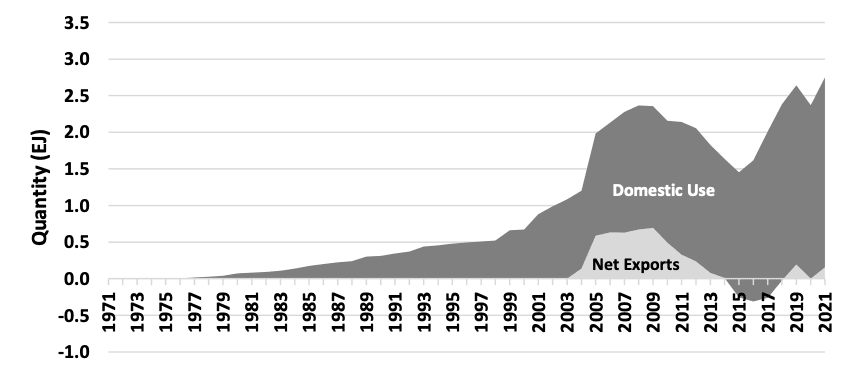

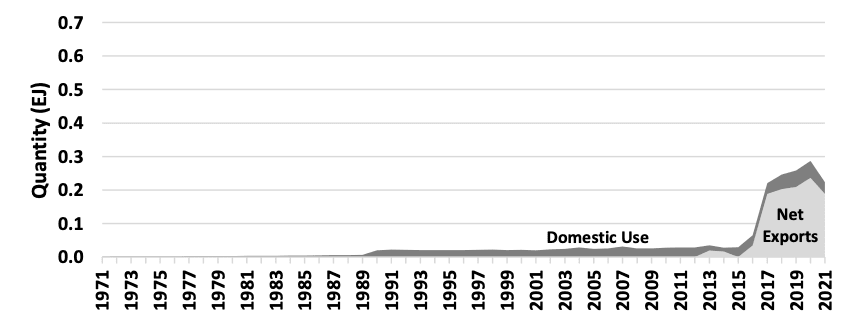

- If production flags, existing domestic consumption is usually prioritized over exports. Egypt returned to net gas imports from 2015-2017 as low domestic gas prices encouraged domestic use and incentives for gas production did not keep up (Figure 1(a)).6 Indonesia has seen an overall decline in gas production in recent years, with exports taking a significant hit as domestic use remains relatively stable (Figure 1(b)).

Policy takeaways on LNG exports and domestic markets

Many country-specific factors influence the trajectory of natural gas development in new producers, including the nature of the natural gas resource, the income level of the country, and the ability of the economy to support gas consumption. However, there are a few broad takeaways for policymakers hoping to piggyback off of LNG exports:

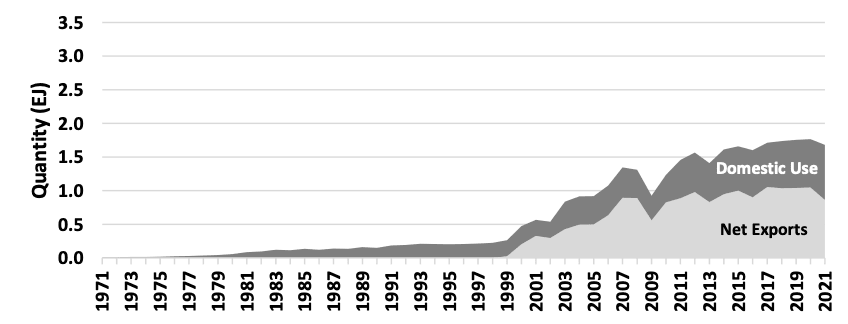

- LNG exports can help support the development of domestic gas markets. Countries like Indonesia, Malaysia, and to a lesser extent Nigeria used LNG exports as a catalyst for domestic gas production, which in turn facilitated the development of a domestic gas market.

- LNG exports are not always a guarantee of strong domestic market development. While it’s still relatively early in their careers as LNG exporters, Angola, Cameroon, and Equatorial Guinea have not yet shown significant growth in their domestic use of gas. This suggests a limited ability thus far to expand the base of gas-consuming domestic customers.

- Industrial users can be anchor customers for the domestic gas market. Two of the biggest success stories for domestic market growth, Indonesia and Malaysia, relied initially on industrial anchor customers in their domestic markets.7 This is usually an easier route to developing a domestic gas market than depending on the power sector.

- Domestic market obligations can spur domestic gas use (but have downsides). Domestic market obligations (DMOs) specify that a certain share of production be reserved for the domestic market. The disparity between domestic and international gas prices means that some use of DMOs may be necessary for governments wishing to stimulate investment in domestic gas infrastructure. For example, Indonesia requires that 25% of the gas produced under production-sharing contracts be allocated for domestic use. That said, DMOs can weaken incentives for upstream investment, with possible negative effects on production.

The value of LNG exports to cash-short countries

Many lower-income countries struggle with large and growing debt burdens. While the development of domestic gas markets is an important goal, the inherent value of LNG exports for shoring up the fiscal stability of these countries should not be neglected. Resurgent rich-country fears about energy security have improved the financing climate for LNG-based gas value chains in lower-income countries, and policymakers in these countries should not hesitate to take advantage of this improved climate to build out LNG exports.

FIGURE 1: Natural gas exports and domestic use for selected non-high-income countries that began LNG exports before 2005. Areas in the charts are additive, summing to total production.

(a) EGYPT (net exports were negative 2015-2017)

(b) INDONESIA

(c) MALAYSIA

(d) NIGERIA

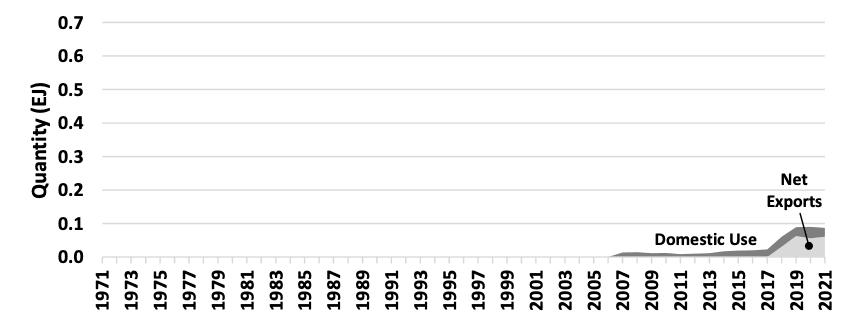

FIGURE 2: Natural gas exports and domestic use for selected non-high-income countries that began LNG exports after 2005. Areas in the charts are additive, summing to total production. (Note: compressed y-axis scale compared to Figure 1.)

(a) ANGOLA

(b) CAMEROON

(c) EQUATORIAL GUINEA

(d) PERU

Endnotes

- Mark C. Thurber and Joseph Chang, “The Policy Tightrope in Gas-Producing Countries: Stimulating Domestic Demand Without Discouraging Supply,” Conference Paper, 2011 Pacific Energy Summit, Jakarta, Indonesia, February 21-23, 2011, https://www.nbr.org/wp-content/uploads/pdfs/programs/PES_2011_Thurber_Chang.pdf.

- Mark Thurber, “Gas-to-Power Value Chain,” September 4, 2018, https://www.energyforgrowth.org/memo/gas-to-power-value-chain/.

- Mark Thurber and Todd Moss, “12 Reasons Why Natural Gas Should Be Part of Africa’s Clean Energy Future,” July 23, 2020, https://www.energyforgrowth.org/op-ed/12-reasons-why-natural-gas-should-be-part-of-africas-clean-energy-future/.

- Neil Munshi, Paul Burkhardt, and William Clowes, “Europe’s Rush to Buy Africa’s Natural Gas Draws Cries of Hypocrisy,” Bloomberg, July 10, 2022.

- Fred von der Mehden and Steven W. Lewis, “Liquified Natural Gas from Indonesia: the Arun Project,” in D.G. Victor, A.M. Jaffe, and M.H. Hayes, eds., Natural Gas and Geopolitics: From 1970 to 2040 (Cambridge University Press, 2006).

- Mostefa Ouki, “Egypt — A Return to a Balanced Gas Market?” OIES Paper: NG 131, June 2018, https://www.oxfordenergy.org/wpcms/wp-content/uploads/2018/06/Egypt-a-return-to-a-balanced-gas-market-NG-131.pdf.

- Mark Thurber, “Gas Markets Usually Start With Industrial Applications,” February 2, 2021, https://www.energyforgrowth.org/memo/gas-markets-usually-start-with-industrial-applications/.