India faces two great challenges: to meet its global climate commitments while simultaneously achieving its development objectives of eradicating poverty, and improving energy access, health, and education. The trajectory of this transition is unprecedented given that no other country with a population so large and so young has had to deal with the challenges of decarbonisation this early in its development pathway.

In order to meet these goals, India’s energy transition strategy includes plans to increase the use of both fossil fuels and renewable energy. The Government of India (GoI) has indicated at various fora that the country plans to increase its renewable energy capacity (from 146 GW today to 450 GW by 2030), increase production of coal (from ~700 million tonnes today to 1.5 billion tonnes by 2030), expand refining capacity of petroleum products (from 250 million tonnes per annum today to 400 MTPA by 2040), and increase the share of natural gas in India’s broader energy mix (from 6% today to 15% by 2030).

This strategy raises questions about the role of natural gas in the country’s decarbonization pathway. Many countries have used natural gas as a bridge fuel in the decarbonization process, so could India do this as well? Natural gas could lead India down a lower emissions pathway, but the political economy of the energy system will likely leave it a marginal player.

There’s no plan to phase out coal for gas in the power sector

Globally, the power sector has seen a coal-to-gas-to-renewable energy transition, driven mostly by economics. This is unlikely to happen in India for several reasons:

- Ingrained coal economy. India has traditionally relied on coal with a domestic capacity of ~200 GW and a production capacity of 730 MT in 2020. This reliance could be increased by recent policy changes, including allowing private companies to mine and sell coal, auctioning 119 coal blocks, and enacting amendments that will make it easier for coal companies to acquire land.

- Non-competitive gas. Domestic production of gas is stagnant and imported LNG is expensive. Costs for more expensive gas can not be recuperated because end-consumer power tariffs are regulated, preventing generators using LNG from passing on associated costs to end consumers.

- No peaking rewards. India does not yet have a peaking power policy that may benefit gas. This has led to stranding more than 14 GW of gas-based capacity.

- India does not plan on using gas to phase out coal. Despite the opportunity that would present for emissions reductions, neither India’s domestic policies nor its first Nationally Determined Contribution (NDC) mention using natural gas for this purpose. Instead, India’s strategy for power sector decarbonization currently hinges on substituting coal and renewable energy, with natural gas playing a small role. India intends to build 450 GW renewable energy by 2030 according to the 2020 planning document produced by the Central Electricity Authority (CEA), India’s electricity regulator. The plan proposes relying on battery storage and pumped hydro to manage variability with minimal contribution from natural gas. In 2030, CEA projects that natural gas will account for only 1.4% of generation (Table 1). During that time, coal’s dominance in electricity generation is expected to erode from ~70% today to 54%.

Gas could still play a role outside the power sector

While the share of gas in the country’s energy mix remains at just ~6-6.5%, niche sectors are driving a steady increase in consumption. Demand is especially rising in sectors where gas can substitute for liquid fuels.

For example, India has been increasing its pipeline and distribution network through policy changes on City Gas Distribution (CGD). This has garnered positive interest and response amongst private players, with significant participation in the reverse auction process. This strategy has seen results (graph 1) as the share of road transport and cooking in total gas consumption is now almost on par with the power sector. Further, the number of vehicles using natural gas as fuel has slightly outpaced overall vehicle growth in the past ten years (11% vs 9%). The number of household connections for cooking has increased at an average of 14% and needs to increase at an even faster pace to reach the GoI target of 50,000,000 households by 2030. The oil and gas regulator is also considering policies that will allow LNG in long-distance freight transport.

Another potential area of growth is the industrial sector, particularly medium, small and micro enterprises (MSMEs). These are typically located in specialized clusters across India (Table 2) and rely primarily on coal, petroleum products and firewood. Air pollution concerns are increasingly forcing India’s Central Pollution Control Board to enforce stricter emission norms, particularly in the northern part of the country, which is likely to drive these industries toward natural gas.

But its growth will depend on external mandates

Substituting natural gas for LPG and firewood in cooking, and for coal and petroleum products in industries will require policy changes on taxation, carbon pricing, and environmental norms to reduce air pollution – India is home to 22 of the 30 most polluted cities. Natural gas is not part of the Goods and Services Tax (GST— a unified taxation code) which applies to coal and most petroleum products. This makes gas costlier than other polluting fuels, since multiple taxes are added at different entry and exit points of the supply chain to the base price of the fuel, limiting its consumption. While the industry has been advocating for its inclusion in the GST, the fear of revenue loss for the state governments has impeded the process. Air pollution is often not monitored, and rules are unenforced, which provides no incentive for polluting industries to transition. Further, most MSMEs lack financial resources to change their supply-chain process which makes them reluctant to shift to gas. Any significant change will involve push and pull policies implemented at the federal level.

What does all this mean for India’s climate strategy?

At the G20 meeting in July 2021, despite pressures to announce a net-zero emissions target year, India invoked the right of developing countries to continue growing and urged G20 countries to lower per capita emissions to the global average by 2030. The country also declined to sign off on phasing out coal by 2025. This stance is compliant with the domestic energy policy of pursuing growth in both fossil fuels and renewable energy to meet the country’s development goals.

But the strategy also means ongoing investments in carbon-intensive infrastructure. For instance, in the natural gas sector alone the country will see investments to the tune of INR 1 trillion in regasification terminals, pipeline infrastructure and Compressed Natural Gas (CNG) pump stations. The number of CNG pump stations has grown at an average of 15% over the past 9 years, and is expected to hit 10,000 by 2030. India is expanding its pipeline network to 30,000 km from 16,000 km today and increasing regasification terminal capacity to 72 MTPA from ~54 MTPA today. Similar investments are being made in coal and crude oil refining.

The scope of these investments suggests that while India will meet its 2015 NDC target of reducing emissions intensity by 33-35% by 2030, the overall decarbonization roadmap is still hazy. The power sector perhaps has the most clarity given the rising share of renewable energy. Transitions in transport and industry however are dependent on a number of policy changes.

Natural gas could help clear some of this haze and help lower emissions, but its role in India’s climate strategy hinges on a series of policy initiatives, without which its role will continue to be marginal.

TABLE 1: India’s projected electricity sector mix in 2030 by the Central Electricity Authority

| 2030 Projected Energy Mix | ||

|---|---|---|

| Fuel Type | Installed Capacity (MW) | Likely Generation (TWh) |

| Hydro (includes imports) | 60,977 | 206.6 |

| Pumped Storage | 10,151 | 4.4 |

| Small Hydro and Biomass | 15,000 | 7.2 |

| Coal + Lignite | 266,911 | 1357.7 |

| Gas | 25,080 | 35.4 |

| Nuclear | 18,980 | 113 |

| Solar | 280,155 | 484.2 |

| Wind | 140,000 | 309.1 |

| Battery Storage | 27,000 |

Source: Report on Optimal Generation Capacity mix for 2029-2030, January 2020, Central Electricity Authority, Ministry of Power, Government of India.

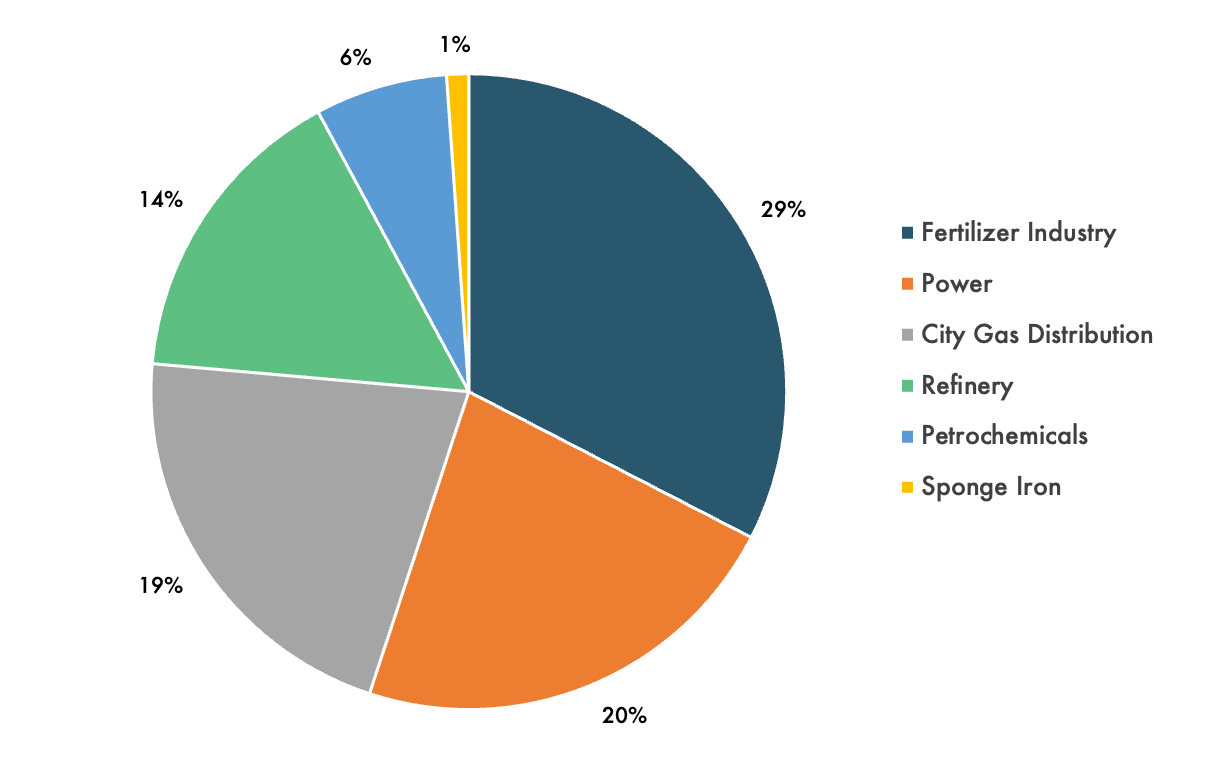

FIGURE 1: Sectoral natural gas consumption in India in FY2020

Source: Indian Petroleum and Natural Gas Statistics 2019-20, January 2021, Ministry of Petroleum and Natural Gas, Government of India.

Note: Others include consumption in industrial and manufacturing, tea plantation, internal pipeline consumption, LPG shrinkage and miscellaneous.

TABLE 2: Major energy sources across clusters in India

| Sector | Cluster | Product/Process | Major Energy Source |

|---|---|---|---|

| Glass | Firozabad | Glass products | Natural gas |

| Brass | Bhubaneshwar | Utensils | Coke/coal, firewood |

| Brass | Jagadhri | Brass, aluminum | Coke/coal, firewood |

| Brass | Jamnagar | Extrusion, foundry, machining | Coke/coal, firewood |

| Brick | Varanasi | Fired clay bricks | Coal |

| Ceramics & refractories | Morbi | Wall tiles, vitrified tiles, sanitaryware, floor tiles | LNG, coal gasifiers, LPG |

| Ceramics & refractories | East & West Godavari | Refractory bricks, ceramic jars | Coke/coal, firewood |

| Ceramics & refractories | Khurja | Ceramics and potteries | Coke/coal, firewood |

| Chemical | Ahmedabad | Chemicals & dyes | Firewood, coke/coal |

| Chemical | Vapi | Chemicals & dyes | Firewood, coke/coal |

| Dairy | Gujarat | Chilling and pasteurization | Electricity, furnace oil |

| Foundry | Batala, Jalandhar, & Ludhiana | Foundry | Firewood, Coke, Electricity |

| Galvanizing and wire-drawing | Howrah | Galvanizing, wire-drawing | Coal, HSD/LDO |

| Ice-making | Bhimavaram | Ice blocks | Electricity |

| Paper | Muzaffarnagar | Kraft paper | Biomass (various forms) |

| Rice mill | Ganjam | Rice | Rice husk, electricity |

| Rice mill | Vellore | Rice | Rice husk, electricity |

| Rice mill | Warangal | Raw rice | Rice husk, electricity |

| Sponge iron | Orissa | Sponge iron | Coke/coal, electricity |

| Tea | Jorhat | Coal and NG-based | Coal and natural gas |

| Textiles | Solapur | Towels and blankets | Coke/coal, lignite, natural gas, electricity |

| Textiles | Surat | Sarees and dress materials | Coke/coal, lignite, natural gas, electricity |

| Textiles | Tirupur | Compacting, dyeing, knitting | Coke/coal, lignite, natural gas, electricity |

Source: As per the BEE study in 2012. Mehta, A. (2021). The Petrochemical and Micro, Small and Medium Enterprises Sectors. In V. S. Mehta, The Next Stop: Natural gas and India’s journey to a clean energy future (pp. 359-389). Harper Collins.