Kenya Power is one of the largest electric utilities in Africa, connecting more than 7.5 million customers.1 Like many utilities the world over, Kenya Power struggles with fully recovering operating costs. This has been compounded by system (technical and commercial) losses which have risen above 26% (2,224 GWh) in the recent past.2 The outcome has been a 92% reduction in profit from US$ 49 million for the year ending June 2018 down to US$ 3 million for the same period ending in 2019 — and COVID-19 is set to exacerbate this.3,4 This impact on service delivery triggered a sustained social media campaign trending under the hashtag #shutdownKPLC. While there are many issues with the utility, KPLC’s financial statements reveal three fundamental problems with their revenue model.5

1. Rapidly expanding connections has cratered revenue per customer

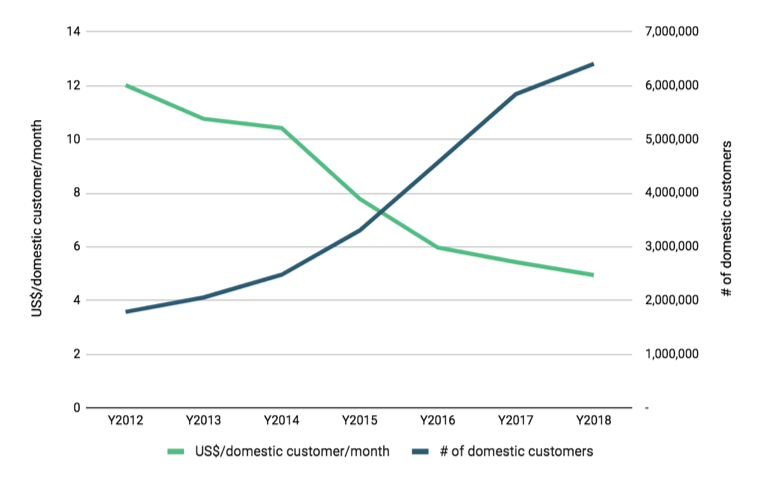

Between 2010 and 2017 Kenya had the highest annual percentage gain in access rates in the world, and more than doubled connections between 2015 and 2019 through an aggressive campaign that included the Last Mile Connectivity Project (LMCP).6 Although this has resulted in an aggregate revenue increase, the net income per customer has been decreasing drastically (Figure 1) and total consumption has increased by a mere 25% in a period that experienced more than a 100% increase in total number of connections. Despite expectations that the aim of achieving universal access by 2022 will in the long run result in nationwide social benefits, so far it has adversely affected the fiscal viability and performance of the utility, thus negatively affecting the main source of electricity needed for powering economic growth.

FIGURE 1: Revenue per domestic customer per month versus total number of domestic customers

2. Declining revenue from core commercial-industrial customers

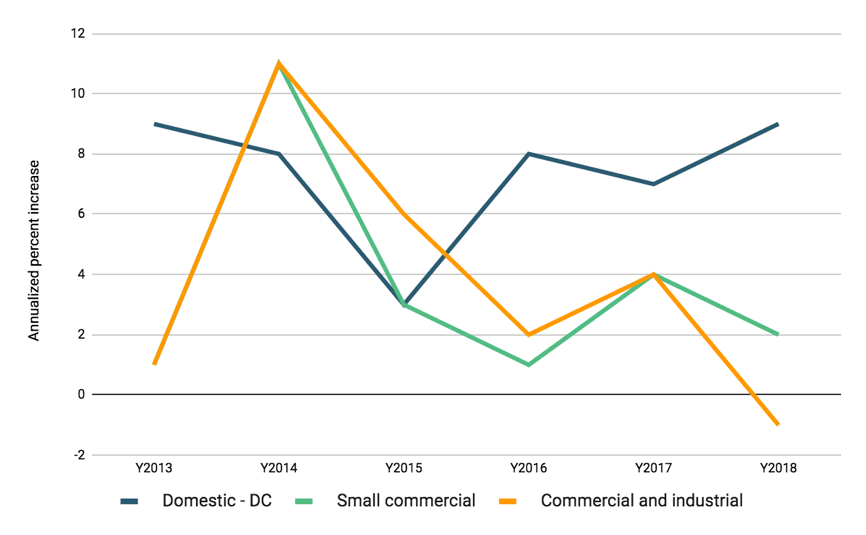

About 700 high consuming, highly profitable commercial-industrial (CI) clients represent barely 0.01% of the total clientele, but over 54% of KPLC’s total sales.7 Yet these anchor CI customers are being driven away from KPLC largely due to the rise in cheaper and more reliable captive solutions, including solar PV (Figure 2). CI customers such as Kapa Oil Refinery Limited, Two Rivers Shopping complex, London Distillers Limited, Williamson Tea, and Garden City Mall have all installed solar PV systems that are larger than 1 MW in peak capacity. Others like Devki Steel Limited have installed coal-fired plants of up to 15 MW. Without this high consumption, reliable customer base, KPLC’s revenue model will quickly become unsustainable. KPLC recognizes this shift and is working hard to maintain and even increase demand from CI customers by building dedicated distribution lines, installing smart meters and fiscal incentives (e.g. ultra-low time-of-use tariffs).

FIGURE 2: Annualized percent increase in total electricity sales (GWh)

3. Declining profits

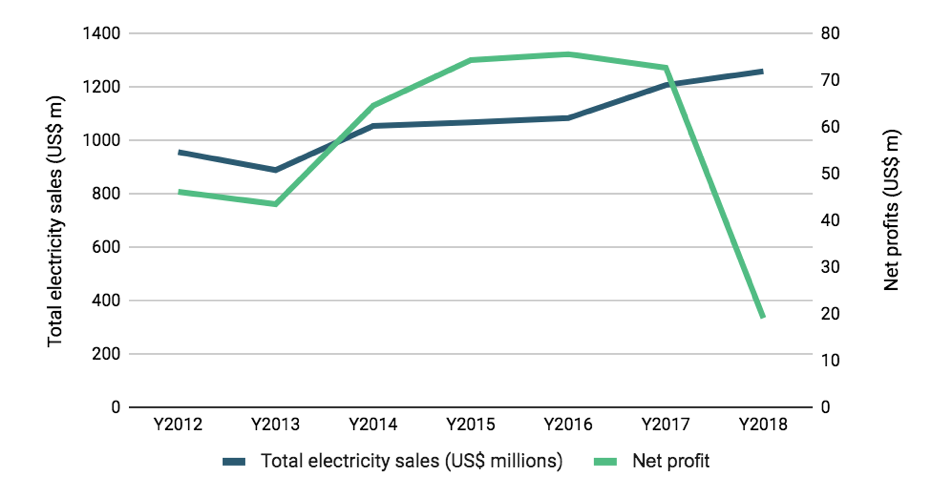

While total revenue per unit of electricity sold has remained steady between US$ 0.14 and 0.16 for the last 8 years, profit has declined drastically (Figure 3). The 92% decline in profit reported for the financial year ending 2019 blew the lid off the utility’s troubles. Cost of sales, mismanagement, system losses (technical and non-technical), rapid expansion, declining revenue per customer, and other factors have eroded the profits. Total debt is reported to be above US$ 1 billion, leaving the utility highly leveraged with a debt-to-equity ratio of 1.8 and with short-term credit exerting unprecedented pressure on cash flows.8 Lack of liquidity will inevitably slow down the power sector modernization plans and affect the delivery of service, which could further propagate the shift to alternative electricity solutions among CI customers. This trajectory could lead to a death spiral.

FIGURE 3: Total electricity sales versus net profits (US$ millions)

Potential solutions

- Expanding and diversifying revenue streams. Besides the physical assets that are currently being leveraged for other revenue sources such as hosting fiber optic cables and street lighting, Kenya Power has long-term records of more than 7.5 million clients with data that could be used as a proxy for credit rating. This database can be used to deliver additional financial services such as asset finance. Diversification of opportunities within the energy sector such as energy advisory, technical services, and energy use analytics provide other avenues for new revenue as well.

- Counterbalancing the influence of government in corporate governance. Even with its current troubles, there is broad consensus among economists and development practitioners that the privatization of Kenya Airways, including partial acquisition by KLM, a strategic partner with industry experience and networks, had an initial positive impact on the firm.9,10 Like all public utilities, Kenya Power is vulnerable to politically driven decision-making processes which may not align with the utility’s longer-term business interests. There needs to be a balance between public sector interests and private sector values to ensure that the utility innovates and remains relevant in the long-term. The current debt could be converted to equity with the Government increasing its stake in the utility, then attracting a strategic partner to acquire slightly less than 50% of its stake in the utility. The final share spread being close to a near-equal tripartite split between shares floated on the Nairobi Stock Exchange, the Government and a strategic investor. This would reduce the exposure to political interest associated with public sector driven electrification programs.

- Demand stimulation. The current load factor is below 75%, but there are many low-hanging opportunities to increase electrification. Converting urban clientele that currently use LPG to power electric stoves by offering ultra-low time-of-use tariffs for cooking (comparable to past preferential tariffs given for water heating) is one area ripe for opportunity. On the same basis, large thermal energy consumers currently using biomass sources for energy including the tea processing industry, cement processors, edible oil refineries, and others can be incentivized to switch part or all of their energy needs to grid-based electricity. Promoting the uptake of electric vehicles also has the potential to increase demand, although marginally. Kenya registered an average 15,000 vehicles per month between 2016-2017.11 Conversion of about 25% of this fleet to electric vehicles has the potential to increase demand by more than 60 GWh,12 and subsequently increase the utility’s revenue by close to US$ 10 million per year.

Endnotes

- Kenya Power official website. https://www.kplc.co.ke/content/item/14/about-kenya-power

- Kenya Power (2018) Annual Report and Audited Financial Statements, Nairobi (pg 208)

- Kenya Power (2019) Annual Report and Unaudited Financial Statements, Nairobi

- Lights dim for Kenya Power shareholders https://energycentral.com/news/lights-dim-kenya-power-shareholders

- Kenya Power Annual Reports and Financial Statements, 2012 – 2019

- IEA, IRENA, UNSD, WB, WHO (2019), Tracking SDG 7: The Energy Progress Report 2019, Washington DC

- Kenya Power (2018) Annual Report and Audited Financial Statements, Nairobi

- Kenya Power (2018) Annual Report and Audited Financial Statements, Nairobi (pg 121)

- Oyieke, Samuel. (2002). Kenya Airways: A Case Study of Privatization. African Economic Research Consortium, Research Papers.

- World Bank. 2008. Kenya: Kenya Airways Privatization (English). Public-Private Partnership Stories. Washington, DC: World Bank Group.

- Data from Trading Economics online data portal (2017) https://tradingeconomics.com/kenya/car-registrations

- Assuming 0.174 kWh/km and 8,000 km as the average consumption per kilometer and total mileage per year. Source: Sierra Rodriguez A, de Santana T, MacGill I, Ekins‐Daukes NJ, Reinders A. A feasibility study of solar PV‐powered electric cars using an interdisciplinary modeling approach for the electricity balance, CO2 emissions, and economic aspects: The cases of The Netherlands, Norway, Brazil, and Australia. Prog Photovolt Res Appl. 2019;1–15.