BLUF: USG support for African power generation has slowed in recent years, roughly mirroring broader market trends. The number of gas or diesel projects beginning construction has remained relatively small but stable over the past decade – while renewable projects dramatically increased, before falling in the last few years. All in all, the pipeline of investment-ready projects is too small. If the US wants to go big on clean energy in Africa, it will need to focus far more on early-stage project support and strengthening markets.

What’s happening: The Biden Administration is busy ramping up efforts to demonstrate its renewed commitment to both Africa and global infrastructure investment. This reflects rare bipartisan agreement on the need to “counter” China in emerging markets, as well as the administration’s attempts to solidify diplomatic and economic relationships in Africa as the continent’s population and influence grow. African clean energy investment supports US development, climate, and national security goals. But are USG efforts matching the ambition?

To answer that question, we looked at three datasets of African power generation projects (larger than 1 MW) that:

- Reached financial close with help (via loans, grants, or technical assistance) from Power Africa.1

- Received financial approval from the Development Finance Corporation (DFC) or by its predecessor agency OPIC.

- Started construction anywhere on the continent – with or without USG support – as compiled by African Energy.

Our 5 big takeaways

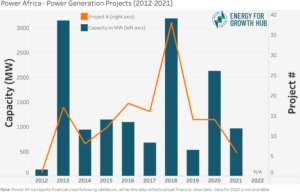

- The number of power generation projects supported by the USG under Power Africa has fallen from a 2018 peak – but the data is messy. Since Power Africa launched in 2013, the number of projects (and total generation capacity) supported by the USG has varied widely from year to year, reflecting market volatility. The spikes in 2013 and 2018 reflect large numbers of transactions in Nigeria and South Africa, respectively. The data is lumpy because the total number of transactions supported in any given year is relatively small, so one large transaction can have significant impacts. Because USAID reports on projects reaching financial close only after verification, we can’t tell yet what’s happened in 2022 – or maybe even in 2021.

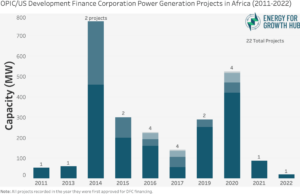

- In the past 2 years, DFC has financed very few African power generation projects – but it’s not a dramatic drop-off. Since January 2021, the only two utility-scale African power generation projects approved for DFC financing were an 87 MW gas plant in Sierra Leone and the refinancing of a 20 MW solar farm in Malawi. This represents a decrease from recent years – but not a huge one. Although expectations are high for DFC to crowd in more capital, historically, DFC/OPIC has never invested in many African energy projects. Since 2011, the most energy generation projects DFC/OPIC has supported in Africa in any one year is four.

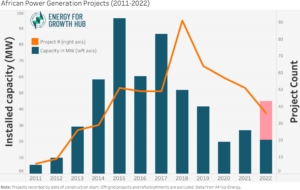

- In part, the slowdown in US support reflects the broader market, in which project development has stagnated region-wide. Data from African Energy shows a recent decline in both the number of projects and the total installed capacity starting construction. (The MW uptick in 2022 is driven by one large nuclear power plant in Egypt, in development since 2015.)[Note: This data counts units at the start of construction, creating a natural lag after financial close. Thus, the financing downturn in 2020-22 could be worse than shown, while a future recovery will also lag.]

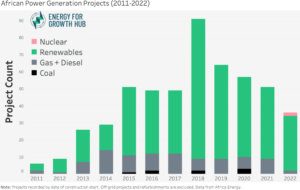

- Construction starts for gas-fired power dropped by half in 2022 – but renewables slowed as well. From this same region-wide data, it is unclear whether the drop in gas financing reflects policies to divest from fossil fuels – or broader energy market conditions. Discerning any impact from US policy is even more difficult: Power Africa data does not yet include 2022 (and 2021 is likely incomplete), while DFC projects show a decline from one to zero, hardly enough to suggest a trend. Regardless, the simultaneous drop in the volume of renewable energy projects belies the argument that development finance can easily be diverted from gas to clean alternatives at the speed and scale required. If there’s no ready pipeline of clean energy projects, there’s little to invest in.

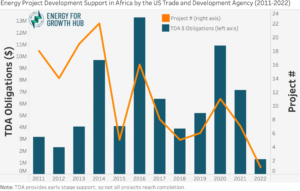

- A pipeline of high-quality, investment-ready projects needs to be built. USTDA is the main USG tool to do so, but its support for African energy is already tiny and has even decreased. Building a competitive pipeline of investment-ready clean energy projects in Africa will take time, risk capital, and often reforms. The US Trade and Development Agency (USTDA) provides early-stage project support, such as grants and technical assistance, to infrastructure projects. This type of support is a principal tool the USG currently has to build a more robust project pipeline. Yet USTDA’s engagement in the African power sector has actually shrunk since 2020.

Bottom line: Africa’s power sector faces structural headwinds that will make investment challenging. If the USG wants to encourage the continent’s energy transition and position itself as a major supporter of African development, it needs to invest far more in project preparation and deploy more early-stage risk capital to help unlock the pipeline.

Endnotes

- These capture projects supported by any U.S. agency (including USAID, DFC, USTDA, MCC, and others), recorded at the date a project reaches financial close. (Power Africa publicly reports financial close following an internal verification process, so their public data may differ from that used here).