Ghana’s discovery of large quantities of oil and gas in 2007 promised to change the face of the country’s energy industry and drive economic growth through export and the development of new electricity generation capacity. Over a decade later, however, the sector is actually losing money while the price of gas remains steep.

Current Gas Supply in Ghana

Ghana’s domestic supply is primarily located in three fields: Jubilee, Sankofa, and Tweneboa–Enyenra–Ntomme (TEN) plus some external supply from the West African Gas Pipeline Company in Nigeria. The Ghana National Petroleum Corporation (GNPC), the state agency responsible for exploration and production of petroleum, currently contracts for 337 MMSCFD (Million standard cubic feet per day) supply to be used in electricity generation and industrial processes. The newly contracted supply of Liquified Natural Gas (LNG) for Tema in 2020 and Takoradi in 2022 will increase total supply to 823 MMSCFD by 2023.

Why are Gas Prices High?

- Low non-power demand. Ghana’s power generators and industries consumed just 255 MMSCFD in 2019. Although this is expected to grow to 448 MMSCFD by 2023 with the new industrialization policies and additional projects from Amandi, Early Power, and Cenpower, excess supply will grow even faster (Figure 1).

- Procurement of additional LNG without linkage to long-term plan. In 2017, the GNPC contracted LNG for Tema in 2020, and Takoradi in 2022 to displace the use of oil and diesel for power generation and anticipate the expected increase in power and non-power demand. These contracts will only further contribute to excess supply.

- Minimal transparency leading to non-competitive contracts. Oil and gas contracts are awarded through direct negotiations, creating rent seeking and poorly negotiated contracts that result in high prices. This non-competitive licensing prevents the public from seeing contracts until after they are fully negotiated and published.

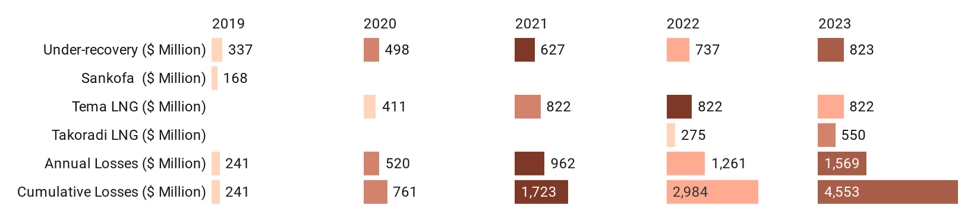

- Significant financial exposure with Take-or-Pay contracts. Take-or-pay contracts mean that the GNPC is paying for supplies that it cannot sell. In 2019 these fees amounted to $168 million. The Tema and Takoradi contracts add an annual $822 million and $523 million respectively so that by 2023, GNPC’s revenue losses will accumulate to $4.5 billion (Figure 2).

- Substantial regulatory and related fees levied on top of the commodity price. The cost of gas is overloaded by several added fees like aggregation, processing and gathering and regulatory charges, that make up another 18.8% of the weighted average cost of gas.

Conclusion

Infrastructure gaps, high non-commodity charges, and underpriced natural gas have led to rapidly rising energy sector debt, threatening the sustainability of the industry as a whole. The GNPC has started to try to unlock East-West supply imbalances by investing in a reverse flow facility to transport excess supply of contracted gas from Takoradi to Tema enclave for expanded power generation. The government also relocated the Karpowership to Takoradi to use excess supply.

FIGURE 1: Natural gas supply and demand in Ghana, 2019-2023

FIGURE 2: Revenue losses of GNPC and additional debt, 2019-2023

Source: Ministry of Energy, 2019.