Why it matters: As emerging energy markets add large quantities of wind and solar, grid-level battery energy storage systems are touted by some donors and development agencies as a zero-carbon “leapfrog” over fossil fuels for energy supply when wind and sun are absent. But unsupported optimism about the near-term potential of batteries to back up renewables on their own may diminish the perceived urgency of investing in other dispatchable alternatives.

The economic value of battery energy storage

Battery energy storage system (BESS) technology provides two broad categories of services to electricity grids:

- Ancillary services to maintain power quality and reliability (batteries as “shock absorbers”). Charged batteries can serve as reserves in the event power generators go offline due to technical issues or maintenance. Batteries are especially well-suited to provide frequency regulation by compensating for small differences in generation and load (demand) on a near-instantaneous basis, helping to ensure that the grid remains stable and customers receive high-quality power that is safe for their electrical devices.

- Time shifting energy to meet demand at a lower cost (batteries as “energy banks”). When wind and solar output are not matched to patterns of demand, energy storage technologies like batteries can “time shift” this energy by storing it when net load (demand minus intermittent renewable output) is low and discharging when net load is high. This obviates curtailment of wind and solar when these renewables are abundant and provides needed energy when they are not. The overall effect is to reduce the cost of integrating wind and solar into the grid by deferring investments in additional generation, transmission, and distribution. (Batteries are not currently cost-effective for the kind of long-term energy shifting that would be required to compensate for seasonal variation in renewable output over weeks or months.)

Mature vs. emerging market context

When it comes to battery deployment, mature and emerging electricity markets have distinctive features.

- Mature markets provide price signals for energy storage. In California, battery owners can bid batteries into markets for both ancillary services and energy. In the energy market, batteries make money by charging when electricity prices are low and discharging when they are high. (Note that this time shifting business model for storage depends on electricity price volatility; as such, it differs fundamentally from the business model for generators, which is to sell the electricity they generate at prices that, on average, more than cover their costs.) Emerging markets generally do not have competitive market frameworks for energy and ancillary services, which means there are no market-derived price signals to incentivize efficient use of batteries for time shifting energy or providing ancillary services, respectively.

- Emerging markets have pressing ancillary services needs and limited capabilities. Inadequate power quality and reliability to support businesses (and improve overall quality of life) is a serious issue in emerging markets [1], and growing wind and solar shares will put the grid under even more stress [2]. In mature markets, by contrast, grid operators benefit from sophisticated technologies and decades of experience that allow them to maintain power quality and reliability with or without batteries.

Insights from California for BESS deployment in emerging markets

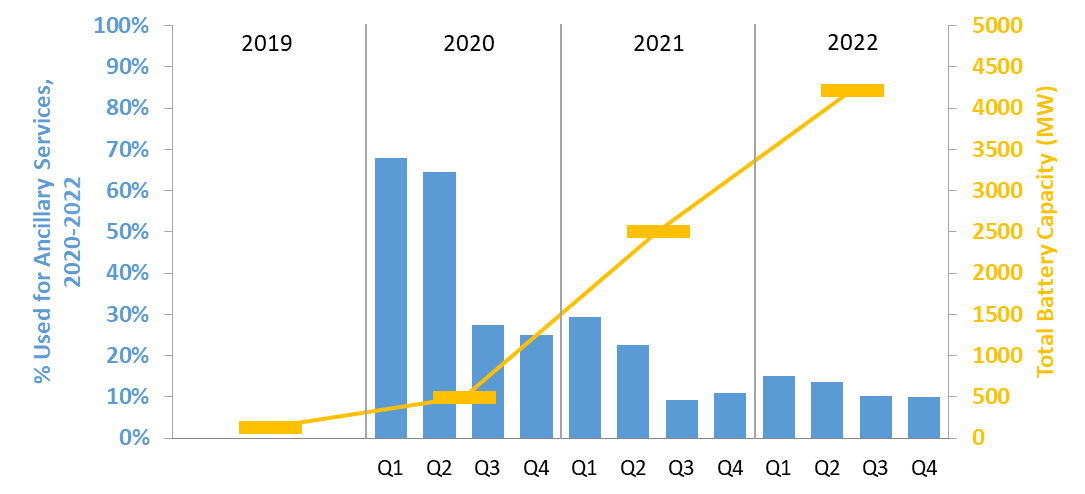

California’s investor-owned utilities were required by the state’s energy storage procurement mandate to build large quantities of storage [3], which spurred the massive growth in battery capacity shown in Figure 1. The costs of these batteries are then recovered in the rates paid for electricity by customers of these utilities. (There is little publicly available data on exactly what the costs were.) Policymakers in emerging markets, where affordability is crucial, might be wise to steer clear of mandated BESS capacity targets like this that do not explicitly weigh the costs of batteries relative to alternatives. But there is still much to learn about viable niches for batteries from California’s large-scale rollout of the technology.

1) Ancillary services are the natural first application for batteries

In a competitive electricity market, ancillary services (and frequency regulation in particular) are one of the more profitable use cases for batteries [4], and at earlier stages of market penetration, that tends to be where they find their heaviest use. As total battery storage capacity increases, the market for frequency regulation becomes saturated, and more of the battery capacity ends up being used to time shift energy. The case of California, which saw massive growth in battery capacity between 2020 and 2022, illustrates this shift. The blue columns in Figure 1 show the significant decline in the share of total battery capacity used for ancillary services between 2020 and 2022.

FIGURE 1: Battery capacity growth in California, 2019-2022 (right axis), and % of capacity used for ancillary services, 2020-2022 (left axis). Data source: California ISO [5].

Emerging markets would do well to emulate mature markets in focusing on frequency regulation as a first niche for grid-scale batteries. This is especially true given these countries’ challenges with grid stability and power quality, which will only become more acute as wind and solar shares rise. Because frequency regulation requires a much lesser total battery capacity than time shifting energy [5], using batteries in this way can provide better initial “bang for the buck” for cash-strapped power sectors.

In line with this logic, countries could consider re-conceptualizing batteries first of all as “shock absorbers” deployed throughout the grid to minimize the impact of single points of failure on grid stability, rather than expensive “energy banks” at which large quantities of energy are deposited and withdrawn to balance wind and solar over the course of a day.

2) Even with massive BESS growth, California is as reliant as ever on dispatchable generation

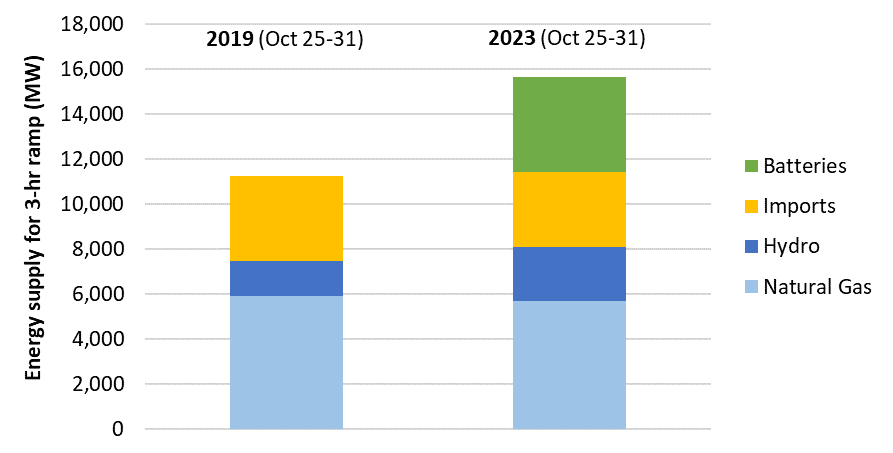

California’s ambitious ramp-up in battery capacity since 2019 has enabled batteries to begin playing an important role in time shifting energy. The state’s huge (and growing) solar capacity means a massive ramp of dispatchable capacity is needed at the end of each day as solar output rolls off (see Figure 2). Batteries are now able to supply more than 4,000 MW of this ramp, but Figure 3 shows how the state’s dependence on natural gas (along with hydro and electricity imports from other states) has scarcely budged between 2019 and 2023. In short, batteries have enabled incremental growth in solar without an expansion of the gas-fired generation fleet—i.e., the green bar representing the power output ramp from batteries is roughly the same size as the growth in the ramping need.

FIGURE 2: Profile of net demand (demand minus wind and solar) in California across one sample day (October 31, 2023). Chart source: California ISO [6].

FIGURE 3: Mix of flexible resources used to meet California’s late-day, 3-hour ramp in net demand. Figure uses average daily ramp (calculated as average of 15:00-16:00 hour to average of 18:00-19:00 hour) for the final week of October in 2019 and 2023, respectively. Data source: California ISO [7].

These market outcomes underscore the degree of difficulty (and cost) involved in trying to significantly expand wind and solar output in the absence of a large existing base of dispatchable resources, such as California’s gas-fired generation fleet. (This is yet another illustration of why “vertical energy transitions” are so much harder than horizontal ones [2].)

Key takeaways for battery strategy in emerging markets

Improve incentives for ancillary services provision. Following the path of mature markets, batteries can find near-term use for frequency regulation in countries that are in desperate need of it, especially as grid stability is challenged by large build-outs of wind and solar. The biggest challenge for emerging market policymakers is to create appropriate financial incentives for batteries to be used in this way in the absence of ancillary services markets (which aren’t realistic to expect in the near future).

Don’t count on batteries alone to back up intermittent renewables! Climate-concerned donors and development agencies may be inclined to push BESS solutions as a “leapfrog” over fossil fuels. In the short term, building BESS technologies might indeed seem like a path of lower resistance than developing gas import infrastructure or, for a country with its own gas resources, building out a robust domestic gas market. But there is a risk that countries will be lulled (including by external cheerleading) into following a path that lands them in an extremely difficult and expensive situation down the road, with significant intermittent generation and no good way to manage it.

The case of California highlights this risk. The state’s energy storage mandate is producing invaluable learning about how best to use batteries in a high-renewables market; it is also a costly “technology push” that has done little thus far to displace existing gas, hydro, and electricity imports in California’s late-day energy ramp when solar disappears. Mature markets still depend on dispatchable generators ramping up when wind and solar output drops off; emerging markets would be prudent to follow their lead rather than attempting the expensive and risky “leapfrog” of hitching future grid reliability solely to batteries.

Endnotes

- Vijaya Ramachandran, “Back to Basics: Tech entrepreneurs in Nigeria need a cheap, reliable and continuous supply of electricity,” Energy for Growth Hub, July 27, 2020, https://energyforgrowth.org/article/back-to-basics-tech-entrepreneurs-in-nigeria-need-a-cheap-reliable-and-continuous-supply-of-electricity/.

- Murefu Barasa and Mark Thurber, “Energy-poor countries face a special challenge: vertical energy transitions,” Energy for Growth Hub, February 7, 2022, https://energyforgrowth.org/article/energy-poor-countries-face-a-special-challenge-vertical-energy-transitions/.

- California PUC, Energy storage, https://www.cpuc.ca.gov/industries-and-topics/electrical-energy/energy-storage.

- Patrick J. Balducci, M. Jan E. Alam, Trevor D. Hardy, and Di Wu, “Assigning value to energy storage systems at multiple points in an electrical grid,” Energy and Environmental Science 11, 2018.

- California ISO, “Special report on battery storage,” July 7, 2023, http://www.caiso.com/Documents/2022-Special-Report-on-Battery-Storage-Jul-7-2023.pdf.

- California ISO, Net demand trend, https://www.caiso.com/TodaysOutlook/Pages/default.aspx#section-net-demand-trend.

- California ISO, Supply data by day, https://www.caiso.com/todaysoutlook/Pages/supply.aspx.