Many countries with electricity shortages—such as Nigeria, Ghana, Mozambique, and Tanzania—have large gas reserves but face challenges developing gas for power.

Gas peaker plants are especially suitable for integration with intermittent renewables

The benefits of natural gas power plants

- Can be built small or large, from 30kW to over 400MW, and run 24/7.

- Different plant configurations, from open-cycle gas turbines (“peakers,” similar to jet engines) to combined-cycle gas turbines, which boost efficiency by utilizing the exhaust heat.

- Can be flexibly ramped up or down based on demand, making them well-suited to backing up intermittent renewables.

- Much cleaner than burning coal (<0.5 tonnes CO2/MWh, vs. around 1 tonne CO2/MWh for coal; negligible SO2, particulates).

- Gas increasingly available through new discoveries, new extraction technologies, and international trade via pipeline or liquefied natural gas (LNG).

in 95% of sub-saharan african countries, utilities do not recover full costs

Constraints to expanded use of gas-to-power

- High upfront capital costs for related infrastructure. Pipelines, LNG transportation (liquefaction, tankers, and regasification), and storage facilities all require billions from government or international investors. There are currently no LNG import (regasification) facilities in sub-Saharan Africa.

- Lack of creditworthy purchasers. Anchor customers are nearly always required, but state-run power companies are notorious for large payment gaps, due both to electricity pricing that does not allow full cost recovery and to difficulties in collection.

- Price distortions. Political pressures to keep domestic gas prices low often causes artificial availability constraints. Preferred uses of gas (for example, fertilizer production in India or city heating in China) may be given first access to cheaper supplies, forcing power companies to turn to more expensive LNG. Some countries index gas to oil prices.

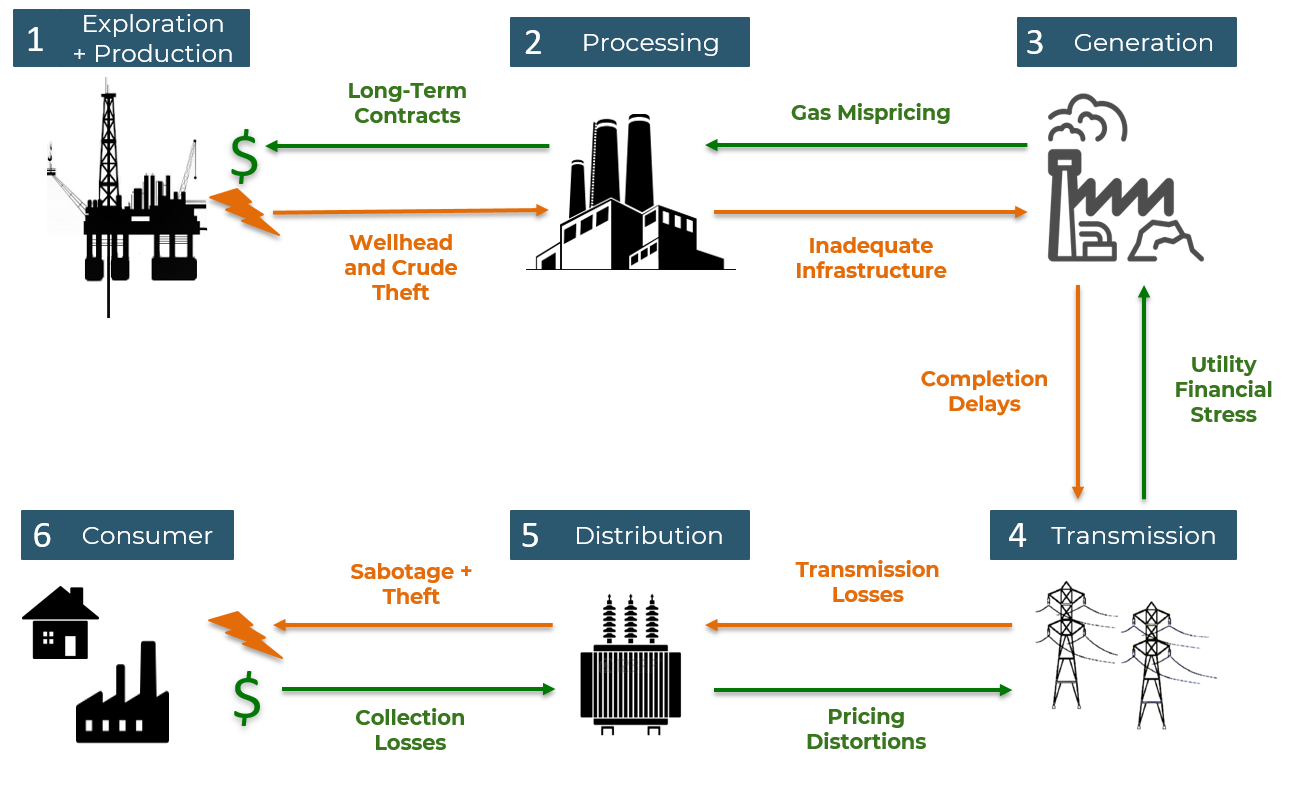

Bottom Line: The gas-to-power value chain can break down in many places and is rarely financially viable if the power sector itself is not (Figure 1). Successful development of domestic gas for domestic power requires careful attention to gas and electricity pricing. International companies and governments may be incentivized to take the more straightforward payout from exports, even where domestic gas use could add more value to the economy.

Figure 1: Challenges in the Gas to Power value chain

Further Reading

- Mark C. Thurber and Joseph Chang (2011), The policy tightrope in gas-producing countries: Stimulating domestic demand without discouraging supply.

- Jorik Fristsch and Rahmallah Poudineh (2015), Gas-to-power-market and investment incentive for enhancing generation capacity: an analysis of Ghana’s electricity sector.

- Donna Peng and Rahmallah Poudineh (2017), Gas-to-power supply chains in developing countries: Comparative case studies of Nigeria and Bangladesh.

- Mark C. Thurber (2016), Why isn’t natural gas in India’s climate strategy?